AlphaFlow @AlphaFlowData

AlphaFlow Joined July 2026-

Tweets23

-

Followers388

-

Following3

-

Likes24

One of the widest disconnects in the market right now: big money is quietly piling $32M into $WULF calls while the stock sits about 35% off its highs. To most people it's a terrible idea to sit in this big of a drawdown, but once you understand how big money actually trades, it makes perfect sense. Institutions run a different playbook than retail. They place large, long-dated conviction bets, focused on where a name is in 6 to 12 months, not tomorrow. That horizon is what lets them hold through the drawdown, and even add into it. That's exactly what's happening in WULF. It's off about 35% from its highs. Any normal trader would've bowed out months ago. But a whale we've been tracking started building this last winter and has pressed it in size twice: about 28,000 contracts ($12M) in April, then another 38,000 ($16.5M) in July after the calls had run to $10 and given it all back. Same conviction, cheaper entry. They're placing a massive bet, even while the stock is nosediving. • Jan-2027 $25 calls • Grown from near zero last fall to 84,000+ contracts • Roughly $32M in premium committed • The April and July adds both landed while the calls round-tripped: doubled this spring, gave it all back as WULF cooled, and they kept adding the whole way down. July 13 alone: ~38,000 contracts, ~$16.5M. WULF recently signed a 20-year Anthropic lease July 6 for~$19B in contracted revenue. A multi-year re-rate, not a tomorrow event. Plenty of retail traders had this same bullish WULF read and still lost on it, because they expressed a 6-month idea with 2-week options. Right direction, wrong duration. When your thesis is structural, your expiration has to be too.

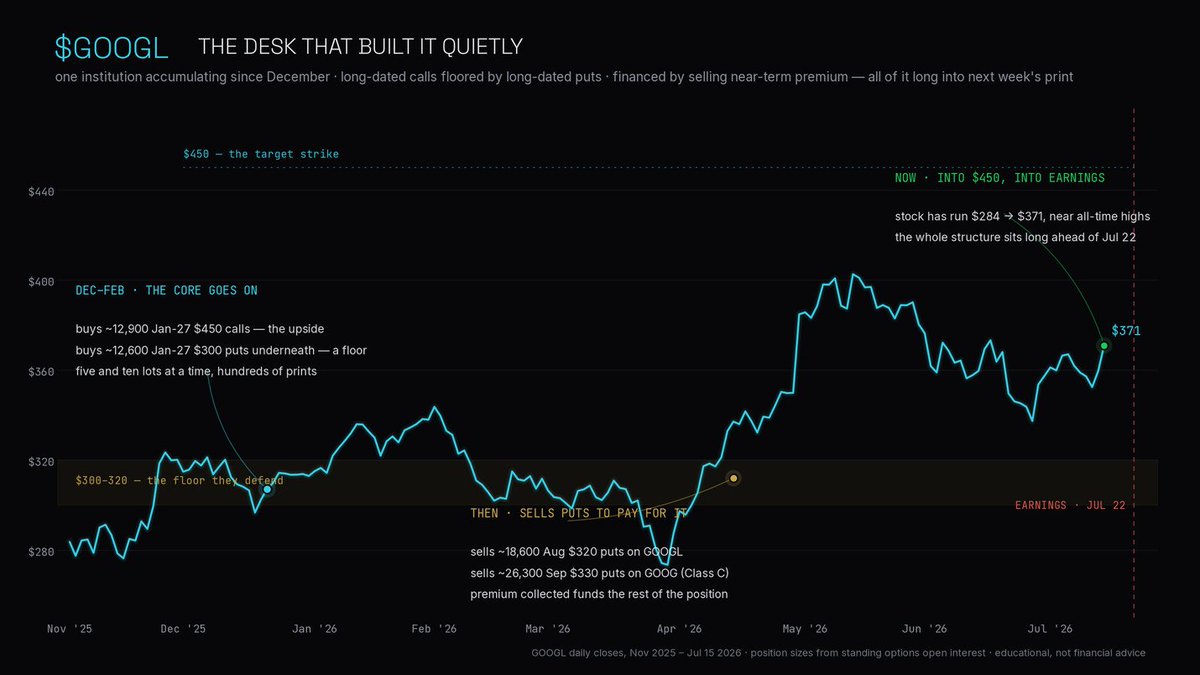

$GOOG reports next week, and everyone's watching whether they will beat after the 100% run over the past year. Two whales are betting yes. One showed up today and rolled its August calls down and out, adding $23M in premium to carry the bet past earnings. The other you wouldn't have noticed — it's spent six months making sure of that. Today's trade first. In three blocks over about seven minutes, one desk sold 42,400 of its August $415 calls and bought the same 42,400 September $410's. Lower strike, a month further out — more delta, more time — and they paid $23M net to press the bet and hold it past earnings. The other whale is the one worth paying attention to. Since December it's put together roughly 12,900 January 2027 $450 calls, never in a size that would catch your attention — five and ten lots at a time, hundreds of times over. And to fund them, it sold the January $300 puts underneath — about 12,600, printed right alongside the calls. Buy the upside, sell the downside to pay for it: a bullish risk reversal, built one clip at a time. It's the same move at every expiry. The desk has written roughly 18,600 August $320 puts on $GOOGL and another 26,300 September $330s on $GOOG, the Class C line. Selling puts on both A and C shares isn't something a retail account does, and the small, repeated lots read like someone working to stay under the radar. So there's no hedge here — just conviction. They've sold every downside strike from $300 to $330 to finance a long-dated bet on $450, happy to own the stock 14% lower or keep the premium if it never gets there. The put-selling carries the same fingerprint as the call-buying, which points to one desk running the whole thing rather than two that happen to agree. Notice what neither of them did. Both chose expiries that sit past July 22. They want to hold into earnings, not trade around it. The tell now is what these desks do after the print.

Everyone who sold $FIG at today's lows didn't read our post.

$FIG was left for dead. Nobody wanted it — until today after it ripped 12%. What most people don't realize: a whale's been quietly accumulating since spring. It started small in late April, and they kept sizing in as the stock fell apart. The position had run ~140% off its

@dan_ennis1 @FL0WG0D x.com/AlphaFlowData/…

$SLS is a small-cap biotech with a whale sitting behind it, and they just made a massive new bet. For weeks one desk has been building calls in SELLAS Life Sciences: nearly $30M in premium, almost 8 million shares of upside, all in the $15 and $30 strikes. Same venue every

@Stock_x1X2cx it was a roll x.com/AlphaFlowData/…

$SLS is a small-cap biotech with a whale sitting behind it, and they just made a massive new bet. For weeks one desk has been building calls in SELLAS Life Sciences: nearly $30M in premium, almost 8 million shares of upside, all in the $15 and $30 strikes. Same venue every

@Christine_een roll x.com/AlphaFlowData/…

$SLS is a small-cap biotech with a whale sitting behind it, and they just made a massive new bet. For weeks one desk has been building calls in SELLAS Life Sciences: nearly $30M in premium, almost 8 million shares of upside, all in the $15 and $30 strikes. Same venue every

$SLS is a small-cap biotech with a whale sitting behind it, and they just made a massive new bet. For weeks one desk has been building calls in SELLAS Life Sciences: nearly $30M in premium, almost 8 million shares of upside, all in the $15 and $30 strikes. Same venue every time, floor-negotiated, both strikes printing in the same millisecond. Today they didn't cash it in. They rolled it forward, straight onto the readout. In a single trade they closed their entire September position, about $15.6M, and reopened the same strikes in January for a $6.95M net debit. $38M of options repriced in one second. SELLAS's lead drug is in a pivotal Phase 3 in AML, and the trial is event-driven. The final analysis triggers on the 80th patient death. They were at 78 in mid-May, and the event rate has slowed to roughly one a month because patients are outliving the model. The 80th event, the unblind, and topline can easily slip past a September expiry. January doesn't have that problem. So they paid $7M to still be holding the moment the data lands, rather than get timed out of a bet they've spent weeks building. From $12.62, the January $15's break even near $21.50, up 70%. The $30's need about $33.80, up 168%. Those are clean-Phase-3-and-takeout numbers.

$FIG was left for dead. Nobody wanted it — until today after it ripped 12%. What most people don't realize: a whale's been quietly accumulating since spring. It started small in late April, and they kept sizing in as the stock fell apart. The position had run ~140% off its spring lows, then gave it all back — an 85% collapse by late June. The whale didn't flinch. Their trades: — ~$3.9M building the position through the spring — ~$2.1M more buying the drop, as the call bled from $4 down to $1 — ~$655K on June 25 alone — the very bottom, buying at a dollar — ~$1.1M more today, into the +12% rip Call it ~$12M in flow, and the position climbed the entire way down while everyone else was bailing. So today it rips +12%, and the degens pile in — $1.7M into $28 calls expiring THIS Friday, swept at the offer, ~18% OTM, four days of runway. Fun to watch. Not where the real story sits. The real story is the whale. More than $6M riding on September calls at today's marks, across two strikes — one of the biggest standing bets in the whole name. What's even more notable, is they didn't take a penny of profit on today's rip. They are in for more upside. This is who we're tracking. $FIG is poised to break out if this run continues, and the whale is your clue. The longer they sit in the position, the more confidence you have that real money is backing the move. Everyone thought $FIG was finished. Somebody with real size has been betting — patiently, through the worst of it — that it's just getting started.

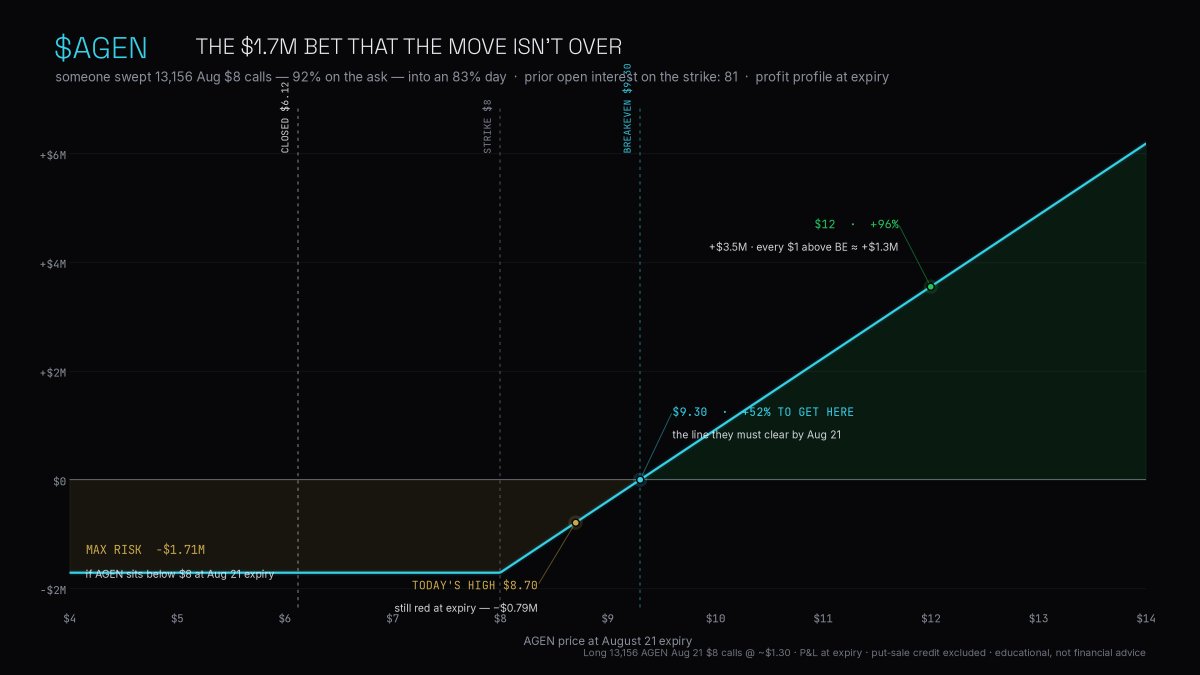

$AGEN ripped 83% today — and notorious pharma bro Martin Shkreli went short. So is the move done? One whale doesn't think so. They spent $1.7M betting it's just getting started. Quick context. Agenus dropped three-year Phase 1b data this morning: 33% overall survival at three years in refractory MSS colorectal cancer, 21.2-month median OS. In a later-line setting where patients almost never last that long, that's roughly double the historical bar. The stock gapped from Friday's $3.35, ran to $8.70, closed $6.12 — on ~174M shares, a massive multiple of any normal day. Then, into that strength, someone with size showed up. They swept 13,156 August $8 calls — 92% at the ask, $1.7M in premium. Breakeven 52% from here, and above today's high. This isn't front-running the news; the news already happened this morning. This is a bet that today was just the first leg. And they funded it with more risk: sold 2,939 August $6 puts on the floor for ~$309K, netting to roughly a $1.4M bullish risk reversal. You only sell the $6 put if you don't think $6 breaks. There's a near-term tell too: 4,350 July $7 calls expiring this Friday. Four days of runway — a bet on follow-through this week. $3M of fresh directional exposure, opened in one afternoon, into an 83% day. Shkreli short on one side. A $3M bull bet on the other.

We heard $INTC is the next SNDK. Good news for bulls: there's a whale that agrees. Someone has been building a monster $INTC long since January, and a month ago they upped the bet — $242M in a single order. The stock topped two weeks later and gave back 22%. The whale didn't blink. And they're not alone: fresh open interest data shows every big bull in this name just re-upped for earnings. Quick backstory. Since at least January, a buyer has been accumulating long-dated calls. Dec $60 and $80 calls. Jan '27 $70 calls. Same trade every time: big size, one clean block cross, bought with the stock in the $40's — strikes that are now 30 to 50 points in the money. Serious leveraged conviction. Then on June 12, 2:29pm, with INTC at $125, they added 63,500 September $97.5 calls in ONE print. $242M bet. No shares attached. Roughly $630M of exposure. Prior open interest on that strike: 154 contracts. After they buy, INTC runs to $142... and bleeds all the way back to $110. Down 22% from the top. They didn't sell a single contract — 70,845 still standing. In fact they added 6,600 MORE at $134 on June 18th. Another single cross, another $28.5M And they're not alone. All through the pullback, a second desk kept buying upside — you can spot them because every print is the same ~13,000-lot size. Jul 2, stock dips to $120: 12,778 July $155 calls in one block. Jul 7-8, stock at $110: 13,300 July $130 calls. Friday, they confirmed their conviction: swapped those July $130's into September $155's — both sides in the same millisecond — and kept the July $155's from the first dip. About $13M riding now, all of it on $155 calls, all of it alive for earnings. The stock is at $110. They're paying for a 40% move. Thursday, someone else opened 5,800 Aug 7 $127/$132 vertical call spreads, and OI confirms it's still standing. Defined-risk money that needs INTC above $132 after earnings. That's +20% from here. And Friday morning a third player, on the floor this time, sold 20,825 August $65 puts near the bid. $1.9M collected on a bet that INTC does not fall apart. September $95 put OI is up ~20x since late May and there's steady call overwriting in the Jan '27s. The big longs are collared, not naked. But you collar positions you intend to KEEP. Someone carried a $630M synthetic long through a 22% drawdown and bought every single dip along the way. Earnings in eight trading days. We're about to find out what they know and whether $INTC will in fact cement itself as "the next $SNDK"

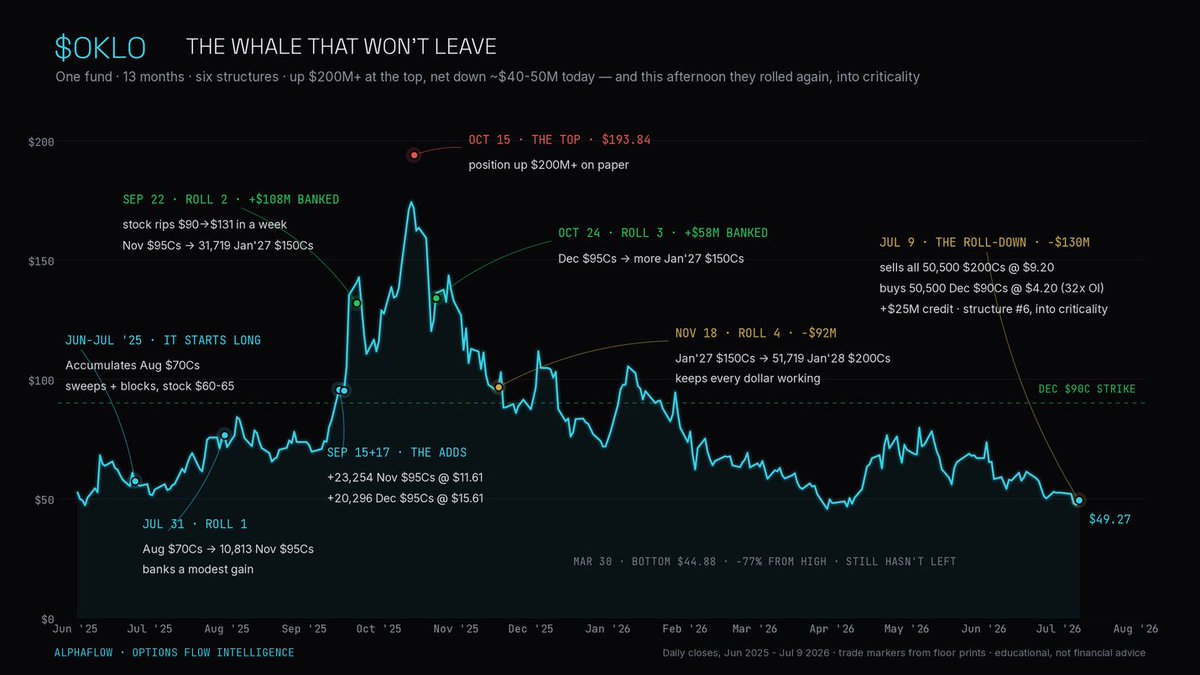

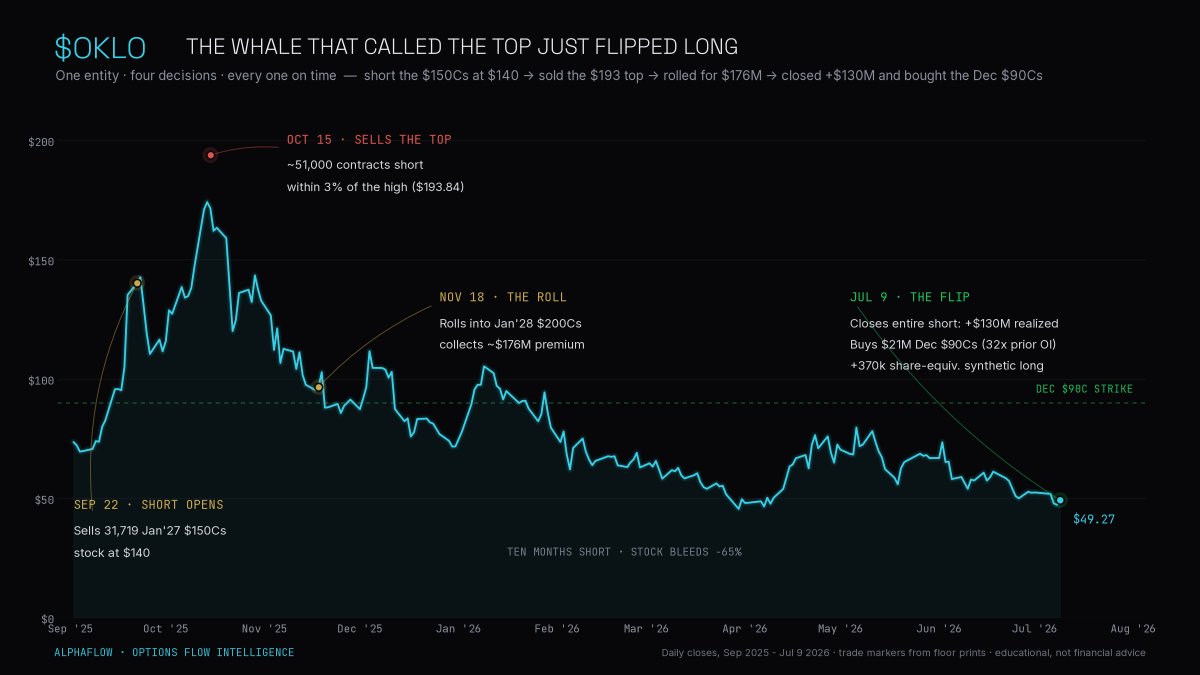

This story just got crazier, and everyone on X (including us) got it wrong. Most people won't believe what I'm about to tell you, because platforms like Unusual Whales show the original $200 calls sold to open. I'm here to set the record straight, with proof. Bottom line: a fund (Susquehanna) lit $200M of paper gains on fire, pulled $25M of premium off the table today, and is STILL positioned for $OKLO to rise. Why everyone got it wrong Every flow platform tags direction off the bid/ask. That works on normal orders. It breaks on negotiated floor packages, where both legs trade at one net price and the desk prints each leg wherever it wants inside the quote. So when 50,500 Jan '28 $200 calls printed at $9.20, top of the day's range, every screen said the same thing: someone urgently bought back a short. Add eight months of OKLO bleeding under the position and you get the story everyone ran with. A whale that shorted the top, made $130M, flipped long. The tags lied. If you want the truth, you have to watch what the market did next. Reading the data instead of the tags Minutes after today's block, the $200 calls collapsed 17%. $9.20 print, $8.30 within minutes, $7.65 close — and the stock actually closed HIGHER than where the block printed, touching +2% at its afternoon high. A call option doesn't lose 17% while its stock goes up unless someone is marking the vol down hard. Dealers short 50,000 calls mark them up. Dealers stuck long 50,000 deep OTM calls mark them down and start dumping risk. The dumping is on tape too. Five minutes after the block, 1,974 of the $250 calls (the strike next door) got hit on the bid. No holder takes profits like that, five minutes after a monster print one strike over. That's the dealer desk that just ate 50,500 calls selling the closest substitute it could find. Desks only do that when they got stuffed long. Which means the customer was selling. The Dec $90 calls did the opposite, firming all afternoon and staying bid into the close. Dealers were short those. The customer bought them. Sold the $200 calls. Bought the $90 calls. This fund added 23,254 Nov $95 calls on Sep 15 '25 with the stock at $90, and five days later the stock was $131. If those calls were short, that's roughly an $80M loss in a week on that add alone. Nobody survives that and calmly rolls up twice. Then there's the SEC. 13F filings show a matching long call block quarter after quarter: ~52,700 contracts on 9/30, ~51,000 on 3/31, tracking the tape-derived position within 1%. Short positions can't appear on a 13F. This one kept appearing. The filer is Susquehanna International Group, CIK 0001446194. Go check EDGAR yourself. They were never short. They were long the entire time. What actually happened A 13-month long-call campaign. Five rolls, six contracts, every leg on tape: Jun–Jul '25 ($60-65): accumulates Aug $70 Cs in sweeps and blocks Jul 31 ($77): rolls into 10,813 Nov $95 Cs, banks a modest gain Sep 15 ($90): adds 23,254 Nov $95 Cs @ $11.61 Sep 17 (~$100): adds 20,296 Dec $95 Cs @ $15.61 Sep 22 ($131.77): stock rips 45% in a week. Sells the Nov $95 Cs @ $45.55, rolls up into 31,719 Jan'27 $150 Cs. +$108M banked Oct 15 ($193.84): stock tops. Position up $200M + on paper Oct 24 ($133.88): sells the Dec $95 Cs @ $46.09, rolls into more $150 Cs. +$58M banked Nov 18 ($96.63): rolls 51,719 Jan'27 $150 Cs into Jan'28 $200 Cs. −$92M Jan 16: trims 1,222 of the $200 Cs @ ~$30 Mar 30 ($44.88): stock bottoms, down 77% from the high Today ($49.27): sells the remaining 50,500 $200 Cs @ $9.20, buys 50,500 Dec $90 Cs @ $4.20. −$130M on the leg, $25M credit on the roll And it's one fund, not six trades. The sizes fingerprint it (31,719 on both legs of the Sep 22 roll; 51,719 on both legs of Nov 18, which is exactly 31,719 plus the 20,000 September add; Oct 24's 19,511 out of the 20,296 bought Sep 17). The stronger proof is simpler: both legs of every roll printed in the same millisecond. One ticket, one entity. So today wasn't a bullish flip. It was a roll-down. Strike drops from $200 to $90, expiration pulls in a year, $25M comes off the table, and the position keeps all 50,500 contracts of upside. Then over the next hour they added ~370,000 share-equivalents of synthetic stock through deep ITM options without ever touching the equity tape. Takeaway Run the full 13 months and it's brutal. A quarter-billion in premium cycled through six structures. +$176M banked on the way up, −$222M given back on the way down. Net down about $46M, from up $200M + at the peak. Most funds walk away from the trade after that. This one dropped its strike, shortened its timeline, and added stock-equivalent exposure into the criticality window. DOE cleared the final safety review July 1. The announcement is due any day. And dealers are now short 50,500 Dec $90 Cs with none of the long $200 C inventory they used to lean on. Any rally forces them to buy into a 145M share float. Thirteen months in, down $45m realized / nearly $200M unrealized, and they just chose more leverage. So either they're going to "make it all back and then some" or someone is getting fired.

Someone spent ten months short $OKLO, made about $130M, and closed the entire position today. Then immediately after they went long with a massive position. Quick backstory. September, with the stock at $140, a trader starts selling calls in size. OKLO tops at $193 on Oct 15

@kyuu47427 Yup and asked some of his friend's to join too!

@TradeLearner11 Because we have built the infrastructure and tools to identify these trades.

Someone spent ten months short $OKLO, made about $130M, and closed the entire position today. Then immediately after they went long with a massive position. Quick backstory. September, with the stock at $140, a trader starts selling calls in size. OKLO tops at $193 on Oct 15 and this account is selling ~51,000 contracts right into the high. In November they roll everything into Jan '28 $200 calls, collect around $176M in premium, then sit there while the stock bleeds to $45. Ten straight months of being right. Today with $OKLO at $49 they bought the whole short back for $46.5M. That's 96% of the open interest on the strike gone in one print. Roughly $130M realized. Now here's where it gets interesting. The same second, same trading floor/venue, they buy $21M into Dec $90 calls. Prior OI on that strike was 1,572 contracts. They bought 50,500. A fresh position and they paid up for it. Then over the next hour they quietly added ~370,000 share-equivalents of synthetic long through deep ITM put sales. Why now? OKLO's first reactor criticality is targeted for this month. DOE cleared the final safety review July 1. There's also a mechanical kicker. Dealers are now short those $90 calls with nothing hedging them, because the $200 calls they were leaning on just got bought back. Any rally and they're forced buyers into a 145M share float. We're witnessing greatness. Question is can they nail this second act.

@snorlax_uw Thanks! Was a tricky one, and really fun to track.

@snorlax_uw You can find the corrected story in my repost I shared yesterday. x.com/AlphaFlowData/…

This story just got crazier, and everyone on X (including us) got it wrong. Most people won't believe what I'm about to tell you, because platforms like Unusual Whales show the original $200 calls sold to open. I'm here to set the record straight, with proof. Bottom line: a fund

@SevenParr It’s a pretty wild story but the initial trade was BOUGHT to open. Not sold.

@muybuenoamigo Ha, yeah that’s the takeaway. They’re still long and not standing down. Also confirmed they are psychos

Jay Hui @jayhui1001

1 Followers 9 Following

Chris Hong @HongChris4134

23 Followers 121 Following

CitizensMatter @citizensmatter1

34 Followers 166 Following

Rajan @rchahall7

428 Followers 795 Following

kaushik @kaushik39516152

48 Followers 41 Following

fullyhedged @hedgemonger

41 Followers 339 Following In an eternal pursuit of the perfect hedge. Just trying not to lose money in the meantime.

Chirag Patel @ChiragP17157288

42 Followers 147 Following

j.a.r.e.d. @jrodpikap

203 Followers 618 Following “The whole aim of practical politics is to keep the populace alarmed by an endless series of hobgoblins, most of them imaginary.” - H.L. Mencken

furkankeless @furkankele63927

1 Followers 55 Following

PokerPat85 @PAllen_Trades

98 Followers 211 Following

Mat B @MathewBrian876

11 Followers 39 Following

CVS Frog 🐸🎥🍿... @CVSfrog

699 Followers 4K Following I’m a frog that lives outside a CVS store (not affiliated). I like stonks. Also a movie buff. $AMC “I've seen the future, I can't afford it…” 😳

jackhansen @jackhansen57062

23 Followers 253 Following

Heavy Chevy 8 @BrianTalley90

3 Followers 200 Following

Wes @Wes_NPC

6 Followers 49 Following

David Ratliff @DavidRa02219234

92 Followers 248 Following

Thomas hire @Carguy1927

2 Followers 20 Following

AiB Capital @AiBCapital

135 Followers 370 Following

வேணாம் @sillymsdian7

5K Followers 2K Following

Chi @NullRepublic

47 Followers 837 Following We are not really here. We are already dead. We are the Null Republic.

raz @Razzy_0123

432 Followers 2K Following

1 @bLAHbLA5LAH

100 Followers 366 Following

Shibani Thakkar @ShibaniTha52403

7 Followers 28 Following

Jack @Jack77161086

15 Followers 88 Following

DisruptiveTech Invest... @vg68961660

18 Followers 116 Following

S Calvert plumbing & ... @s_calvert_heat

3K Followers 1K Following Plumbing and heating specialist, commercial gas/lpg, domestic gas/lpg, oil and renewables

Shanks @monkeyDluffffey

64 Followers 924 Following

GC @CabelloGab36751

0 Followers 9 Following

Maisondelaplage @maisondela38939

274 Followers 6K Following

liangege @liangege27774

34 Followers 649 Following

Stew White @stewputih

214 Followers 700 Following

Jeremy Maine @JeremyMaine4

82 Followers 412 Following

Misha @Misha1192943

66 Followers 449 Following

Tum Rogers @tumrogers74

258 Followers 5K Following

zzzgameshow @FibLevels618886

816 Followers 5K Following

Robert Shaw @RobertShaw1222

10 Followers 200 Following

Brian @Brian39200181

5 Followers 136 Following

RoD🔥 @Rod2ZEROnBACK

1K Followers 505 Following Clinical Psychologist and Options Trader. #SPX #ES #TSLA #NVDA #Bitcoin https://t.co/PoHf6m5xZY

ToRo’s charts 🐒 @ChartsToro

957 Followers 1K Following Student of the markets. Charting for fun. *This is not investment advice*

choose @ELKscape

538 Followers 976 Following break through normal convention, freedom from bubbles, eternal builder, learner, optimist, contrarian, finding the joy in life

Omar Tayar @OmarTayar

197 Followers 4K Following

Rich Off Stock Tips �... @RichOffStock

102 Followers 175 Following Just a dude trying to get rich off the stock market 💰

Matt Carnes @Carnes_Matt

108 Followers 352 Following Former NHRA Top Fuel Crew Member Turned Land Surveyor With An Addiction To Market Structure Analysis

KK @kokispapagalos

1 Followers 50 Following

Tiffany @TiffanyXie10

431 Followers 320 Following

Miao @miaoooni

0 Followers 39 Following

Alpha Pod Trading @alphapodtrading

7 Followers 1 Following

Kairos @Kairosalgo

325 Followers 2 Following Algorithmic trade signals powered by flow, technicals, and price zone scoring. Every trade posted. Built by @kasm_capital

KASM @KASM_Capital

7K Followers 123 Following Former BLK analyst. Perpetual learner. 0dte SPX expert. Sharing options flow, charts, & tradesYou might like