Vaibhav Joshi @InvestWithJoshi

Everyone loves a stock after 5x. I like businesses before they become Twitter threads. Investor 💰 Disc- Don't Buy or Sell on tweets (I'm Biased) Joined December 2018-

Tweets2K

-

Followers3K

-

Following198

-

Likes1K

I wanted to play the MFI recovery, but neither Arman nor CreditAccess gave me enough valuation comfort. Fusion and Spandana were simply too shitty. That's when I came across Satin. Hardly anyone on Twitter was talking about it, coverage was almost non-existent, and the valuation made no sense relative to the business. I spent weeks studying the company, wrote multiple threads on it, and accumulated a meaningful position at much lower levels because I believed the market was mispricing the business. Then came the rerating. The Q1 FY27 update only strengthened my conviction. Asset quality continues to improve, collections remain healthy, profitability is holding up well, and management commentary suggests the recovery is on track. Despite the sharp rally, Satin still looks inexpensive compared to its earnings potential. I believe once it decisively crosses ₹300, momentum traders and institutional investors could drive the next leg of the move.

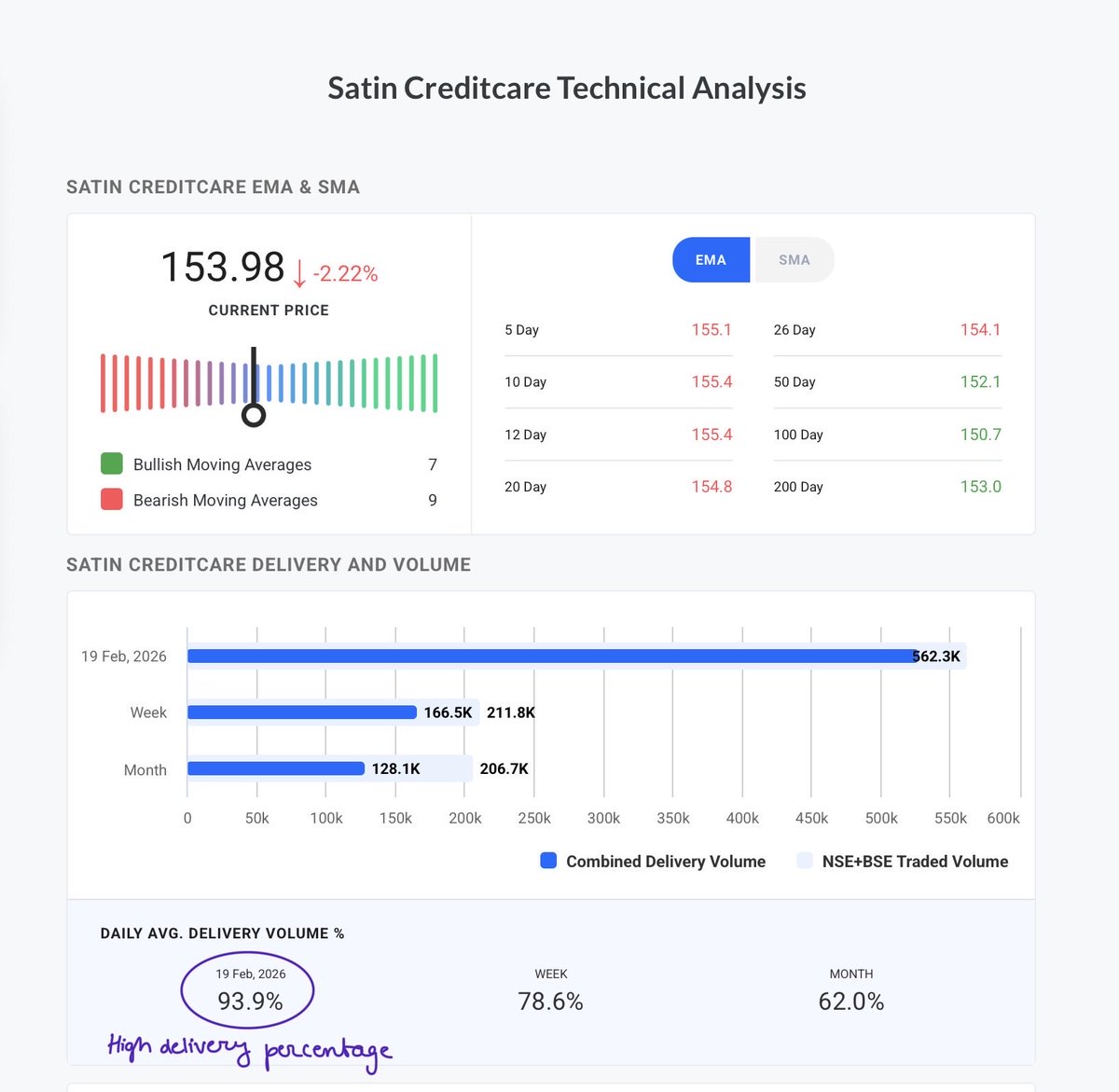

Smart money is quietly loading up on Satin Creditcare Network Ltd 👀 Stock is basing at ₹150–155 with price hugging 50/100/200 EMAs — classic accumulation structure. Massive 93.9% delivery + ₹7.75 cr block buy (5L shares @ ₹155) confirms strong institutional absorption.

@Arghyadip99 They had one of the best asset quality in the peer group and yet are trading at discount. That's where real money is made.

The Singla brothers are executing ruthlessly, turning Prime Cables into a growth machine. 🔥🔥 Massive Tailwinds for the sector.

I always say that guidance alone is never a good reason to invest, especially in SME companies. But when valuations are reasonable, the sector has strong tailwinds, and the promoters appear sensible, sometimes you need to take a calculated leap of faith. The cables space is

@patnaiksatish84 @Arghyadip99 Still 3 quarters are left it will be interesting to attend the H1 con call, maybe the management will revise the guidance but even if they are able to do 160-170 stores it would be good.

@EquityInsightss Funny thing is just look at the Mcap of both, market underestimates Satin a lot. Soon this gap will close.

Satin Creditcare continues to execute exceptionally well 🔥 The biggest positive isn't just the ~27% YoY AUM growth to nearly ₹16,000 Cr or 54% jump in disbursements. It's the quality of growth. Credit cost has come in at just 2.5–3%, below annual guidance, GNPA has improved to 2–2.5%, collection efficiency is back at ~99.9%, and the non-MFI book has expanded to 19%. After one of the toughest cycles the industry has seen, Satin seems to be coming out stronger than ever. If this execution continues I believe the market will eventually rerate the business.

Why I believe India's real estate prices are likely to remain elevated for a long time: As long as black money and unaccounted wealth don't find alternative avenues, a significant portion will continue flowing into real estate. Poor urban infrastructure limits the supply of truly desirable locations, and there is no quick fix in sight. Economic opportunities remain concentrated in a handful of cities, creating persistent demand in those markets. Perhaps the biggest factor is psychology. A large section of Indians genuinely believes that property prices only go up, and that belief itself keeps demand alive. As long as these structural factors remain, expecting a sharp and sustained correction in residential real estate may be optimistic.

@VIP34388096 I have covered it multiple times in last 4-5 months. Its Just people start interacting with the posts when the stock becomes popular and Algo pushes it further.

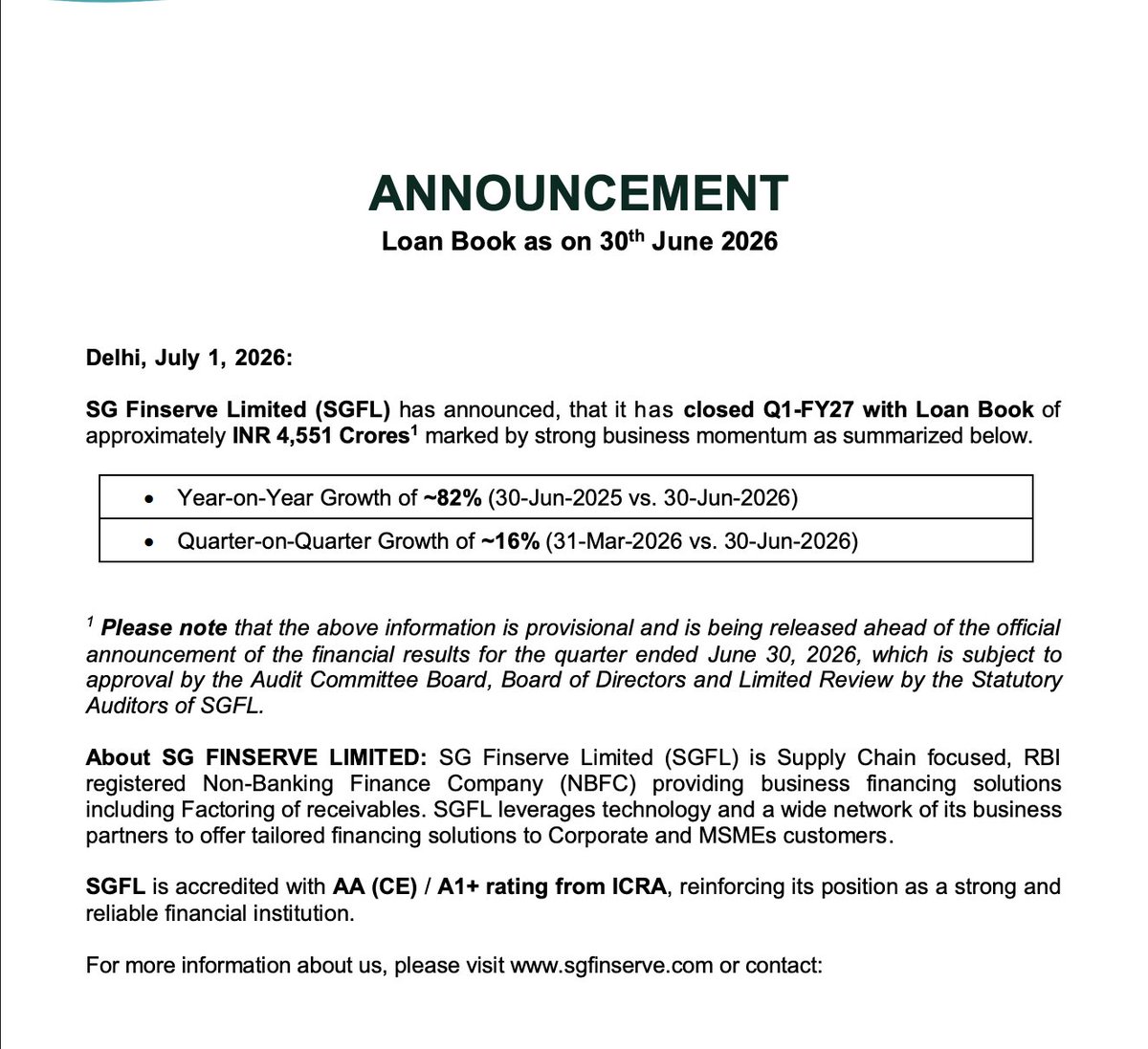

In January 2026, management said they would hit ₹6,000 Cr AUM by March 2027. Six months later, they are already at ₹4,551 Cr. Growing 82% year-over-year. Running ahead of their own guidance. And they have done all of this while maintaining something that should be statistically impossible in MSME lending. Zero NPAs. Not 0.5%. Not 0.1%. Literally zero. Seven consecutive quarters. ₹60,000 Cr disbursed. Not a single rupee written off. The company is SG Finserve. And the reason it can pull this off while management keeps overdelivering on every metric is the most elegant financial mechanism I have come across in Indian NBFCs. ━━━━━━━━━━━━━━━━━━━━ In 2021, the promoter family behind APL Apollo Tubes (India's largest structural steel tube maker, 55% organised market share, 800+ distributors, 50,000 retailers) quietly acquired a dormant NBFC shell called Moongipa Securities. They renamed it SG Finserve. And turned it into a dedicated supply chain financing engine for the massive APL Apollo dealer network. The idea was simple. APL Apollo's dealers need working capital to buy steel tubes. Banks will not lend to them easily because they are small, asset-light MSMEs with no collateral. So SG Finserve steps in. But here is the twist that makes this different from every other MSME lender. ━━━━━━━━━━━━━━━━━━━━ When a dealer needs ₹50 lakh to buy inventory, SG Finserve does not send the money to the dealer's bank account. It pays APL Apollo directly. The dealer never touches the cash. This eliminates end-use risk completely. Now the killer part. If the dealer delays repayment to SG Finserve by even a day, APL Apollo immediately cuts off all future supply to that dealer. Think about what that means. A steel dealer who depends on daily inventory to survive. Whose entire livelihood flows through APL Apollo's products. The punishment for delayed repayment is not a phone call from a recovery agent. It is instant business death. So SG Finserve's dues sit at the very top of the dealer's payment priority. Above rent. Above statutory dues. Above everything. This is not traditional underwriting. This is financial engineering that converts business dependency into repayment certainty. The loan rotates every 45 days. In Q4 FY26 alone, they disbursed ₹7,700 Cr against a book of ₹3,936 Cr. The entire capital base churned twice in one quarter. ━━━━━━━━━━━━━━━━━━━━ The latest numbers tell the story. → AUM: ₹975 Cr (Mar 23) → ₹3,936 Cr (Mar 26) → ₹4,551 Cr (Jun 26) → Revenue: ₹41 Cr (FY23) → ₹334 Cr (FY26) → PAT: ₹18 Cr (FY23) → ₹128 Cr (FY26) → Q4 FY26 PAT: ₹42.27 Cr (+78% YoY) → Return on Assets: 4.8% → Return on Equity: 12% → Gross NPA: 0.0% → Gearing: 1.9x (conservative, ceiling is 3x) Per the Q4 FY26 results press release and management commentary on the April 2026 investor call. That 4.8% RoA is not a typo. For context, UGRO Capital does 1.9% RoA with 2.4% bad loans. Northern Arc does 2.9% with 0.9% bad loans. SG Finserve generates the best profitability in the space while spending nothing on credit costs. ━━━━━━━━━━━━━━━━━━━━ How does it borrow so cheaply? This is the second trick. SG Finserve on its own is rated CRISIL A+. Decent but nothing special. But its actual bank facilities carry a CRISIL AA rating with a Credit Enhancement tag. That CE comes from an irrevocable corporate guarantee by S Gupta Holding Private Limited, which owns roughly 27% of APL Apollo Tubes. That APL Apollo stake is worth ₹10,000 to ₹14,000 Cr depending on the market. It backstops a debt book of roughly ₹2,774 Cr. The cover ratio is 4 to 5 times. Result: SG Finserve borrows at 8.5%. In the MSME NBFC space. Where peers pay 10 to 11%. That 150 to 250 bps advantage drops straight to the bottom line. Every single quarter. It is a structural cost moat that competitors cannot replicate without their own billionaire promoter guaranteeing their debt. ━━━━━━━━━━━━━━━━━━━━ The January 2026 factoring license changed the growth trajectory entirely. Before that, SG Finserve could only do dealer finance downstream of anchor companies. After the license, it can now buy receivables from vendors, participate on RBI's TReDS platform, do invoice discounting on open accounts. The timing could not be better. Union Budget 2026-27 mandated all CPSEs to join TReDS. RBI's June 2026 Master Direction added credit guarantees and liberalised the framework. TReDS platform M1xchange crossed ₹1 trillion annual throughput this year. Management has 28+ anchor tie-ups now and guided that 75% of future growth will come from third-party non-APL Apollo anchors. The factoring arm was the primary driver behind that 82% AUM growth in Q1 FY27. ━━━━━━━━━━━━━━━━━━━━ The valuation math. At ₹674, market cap is roughly ₹4,440 Cr. → Trailing P/E: 34.7x → P/B: 3.0x → Book value per share: ₹225 Management target for FY30: ₹7,500 Cr AUM and ₹500 Cr PAT. If they hit ₹500 Cr PAT by FY30 (a 30-35% CAGR from here), the stock at today's price would be trading at roughly 9x forward earnings. That is Bajaj Finance territory growth priced at PSU bank multiples. Promoters hold 52.9%. Ashish Kacholia holds 1.14%. Madhusudan Kela acquired 9.5 lakh shares at ₹350 average in March 2025 (per BSE bulk deal data). These are not dumb money investors. No institutional analyst coverage exists today. TipRanks confirms zero ratings in the last 3 months. This stock has not been discovered by sell-side research yet. When it does get covered (likely as market cap scales past ₹5,000-6,000 Cr), that itself becomes a re-rating catalyst. ━━━━━━━━━━━━━━━━━━━━ Now the risks. And they are real. Eyes wide open. → APL Apollo just reported Q1 FY27 volumes DOWN 6% YoY to 745kt (missed 875kt guidance badly). Dealer destocking plus HRC price volatility. If dealers are sitting on unsold inventory, the stop-supply threat loses its coercive power → Extreme concentration. The company was literally built to finance APL Apollo's network. If steel or construction enters a severe downturn, anchor health and SG Finserve unwind simultaneously → The zero NPA record is only 3 years old. Never tested through a full credit cycle or systemic liquidity crunch → The 8.5% cost of funds depends entirely on the SGHPL guarantee. If APL Apollo's stock crashes 60-70%, the cover ratio collapses and a rating downgrade inflates borrowing costs overnight → Shares outstanding grew 17% last year via warrant conversions. EPS was flat from FY24 to FY25 despite PAT growth because dilution absorbed the gains → The ₹400 Cr subsidiary plan (ARC, AIF, insurance broking) is unproven diversification into intensely competitive segments with different operational DNA ━━━━━━━━━━━━━━━━━━━━ But here is why I keep coming back to this. India has a ₹30 to 40 lakh crore MSME credit gap. SG Finserve's ₹4,551 Cr book is a rounding error in that market. The factoring license plus TReDS regulatory tailwinds just opened a massive new runway. The balance sheet has room to go from 1.9x to 3.0x gearing without any new equity raise, which alone supports 50%+ AUM growth. A 4.8% RoA company with zero credit costs and a structural borrowing advantage. Growing AUM at 75-82% annually. With smart money backing and zero institutional coverage. The risk is concentration. The reward is a potential compounder hiding inside a corporate supply chain that moves ₹25,000 Cr of invoices per year. I am watching APL Apollo's volumes closely. If the dealer network stays healthy through this soft patch, the thesis only strengthens. If it does not, I will reassess. Not advice. Do your own work on this. Save this. Come back after Q1 FY27 full financials are published.

@mkashipathi I prefer Quality over quantity.

Yet another business that underpromises and overdelivers. My only regret is not loading up on more shares.

Started with just ₹1 lakh from his father's retirement gratuity in 1990. No business legacy. No family empire. No institutional backing. Built a ₹15,000 crore AUM lending institution from scratch. That's what a first-generation entrepreneur can achieve. Dr. HP Singh.

I do it 10 times better than competitors who have big names and large funds behind them. But they get the recognition, the bouquets, the premium valuations. Because there is no big daddy behind me. They forget I do it on my own. They do it on the crutches of their pedigree. That

@Chrisjoe989 Mumbai Metro Line 4 (Green Line).

A metro line is about to cut Thane-to-BKC travel from 60+ minutes to 25 minutes. And one company owns 40 acres of unlaunched land sitting directly on that corridor. At zero cost. Metro Line 4 (Wadala-Thane) is commissioning in FY27. Thane property values already up 40% since 2022 just on anticipation. Historically, metro openings in MMR add another 15-25% ASP uplift within 18 months of going live. That 40 acres has ₹9,700 Cr of revenue potential. The land was inherited at historical book value. Effectively free. The company is Raymond Realty. And it can still grow multifold from here even after giving 100% returns in 3-4 months. I was lucky enough to grab this at ridiculously cheap levels post-demerger when forced selling pushed it to ₹349. The business was firing on all cylinders. But when Raymond Ltd split, its existing shareholders (mostly large-cap textile/conglomerate investors and funds) suddenly received shares of a small-cap real estate company they never signed up for. Their fund rules literally do not allow them to hold small-cap real estate. So they dumped it. Not because the business was bad, but because they were forced to sell by their own investment mandates. That created the gift. And the story is far from over. ━━━━━━━━━━━━━━━━━━━━ Q1FY27 just dropped yesterday. The numbers are insane. → Pre-sales: ₹700 Cr (+129% YoY vs ₹306 Cr in Q1FY26) → Collections: ₹550 Cr (+47% YoY) → No new residential project launched this quarter 129% pre-sales growth in a quarter with zero new launches. That is pure organic demand on existing inventory. Brand pull, not launch hype. Management confirmed performance is entirely in line with forecasts and they remain on track for 17-19% EBITDA margins for full year FY27. ━━━━━━━━━━━━━━━━━━━━ At ₹638, this still trades at 14x earnings with 22% ROE. Peers: → Godrej Properties: 31x P/E, 10% ROE → Sunteck: 23x P/E, 6% ROE → Keystone: 67x P/E, 3% ROE Cheapest valuation in the entire listed MMR real estate space. With the best return on equity. That gap will close. ━━━━━━━━━━━━━━━━━━━━ Here is what the market is still not pricing in. 100 acres of land in Thane at zero cost. 60 acres already under development. The remaining 40 acres (the metro corridor land) have not even been launched yet. Market cap is ₹4,300 Cr. The unlaunched land alone could be worth more than the entire company today. On top of this, 7 JDAs signed across Bandra, BKC, Wadala, Sion, Mahim, Kandivali. Combined GDV: ₹17,000 Cr. Zero land capital deployed. Pure asset-light model. Total pipeline: ₹42,000 Cr revenue potential. Market cap: ₹4,300 Cr. 🔥 ━━━━━━━━━━━━━━━━━━━━ The execution is backing it up. → FY26 pre-sales: ₹3,023 Cr (+31% YoY) → Q4FY26 pre-sales: +139% YoY → Q1FY27 pre-sales: +129% YoY (momentum sustained) → JDA mix hit 54% of pre-sales, two years ahead of guidance → Revenue growing at 20% CAGR through FY29E → EPS path: ₹46 (FY26) → ₹87 (FY29E) ━━━━━━━━━━━━━━━━━━━━ Risks exist. → 100% MMR concentration → JDA approval delays (society consents, SRA/MHADA) → Competition from Lodha/Godrej/Oberoi → Net debt at ₹827 Cr (up from ₹380 Cr YoY as construction peaks) Eyes open on those. ━━━━━━━━━━━━━━━━━━━━ But the risk-reward at this valuation is skewed heavily in one direction. A ₹42,000 Cr pipeline company trading at ₹4,300 Cr market cap. Proven execution. Cheapest multiple among peers. 129% pre-sales growth in the latest quarter. The first 100% was the demerger discount closing. The next leg is earnings compounding at 24% CAGR and the market waking up to that free land sitting on a metro corridor about to go live. Per Arihant Capital's initiating coverage (July 2026), NAV-based target is ₹1,025. Still 63% from here. Not advice. Do your own work on this. But I am not selling a single share anytime soon. Save this. Come back after full Q1FY27 financials are published.

I do it 10 times better than competitors who have big names and large funds behind them. But they get the recognition, the bouquets, the premium valuations. Because there is no big daddy behind me. They forget I do it on my own. They do it on the crutches of their pedigree. That is HP Singh. Founder of Satin Creditcare. I was listening to a year-old podcast of his today and this hit different. Because the stock market is literally proving him right. → CreditAccess Grameen (European parent): 3.2x book value → Fusion Finance (Warburg Pincus backed): 1.5x book, barely broke even in FY26 → Satin Creditcare (self-made, no backer): 0.83x book, while generating 12.3% ROE and 79% profit growth Same industry. Same borrowers. Same cycle. The one without pedigree trades below its own net worth. Who is HP Singh? Started with ₹1 lakh of his father's retirement gratuity in 1990. Built a ₹15,000 Cr AUM lending institution from scratch. No legacy, no lineage, no fund backing. First generation. During demonetization, 74% of the portfolio got hit. ₹1,200 Cr at risk against ₹683 Cr net worth. Every analyst said Satin will vanish. His words: I did not sleep for a year and a half. I did not know what eating meant. I was like a zombie. With one hope in mind. I will not fail. I will not go out of business. Put ₹90 Cr of his own money in. Called every branch manager personally for a year. Dragged collections from 20% back to 99%. Satin survived. Now he just announced ANOTHER ₹100 Cr infusion at current prices. Raising stake from 36% to 38%. He also said: I will not let anything happen to this company. That is the difference. They have someone to come save them. I will never need saving because I will never let it go wrong. This is my hard-earned money. My prestige. My reputation. The business is backing him up. → Q4 FY26 PAT: ₹162 Cr (vs ₹22 Cr year ago, +630%) → Full year PAT: ₹332 Cr (+79% YoY) → AUM: ₹15,174 Cr (+19%) → Credit costs falling: 4.6% FY25 → 3.6% FY26 → 2.2% in Q4 → Diversified into housing + MSME (17% of book now secured, was 6% two years ago) → Zero equity dilution since the structural pivot → FY30 AUM target raised 28% to ₹32,000 Cr The old Satin (pre-2023) deserved the discount. 41% book in one state. Diluted 16 times. Bled in every crisis. The new Satin is in 26 states. Has a secured buffer. Handled the FY25 sector stress better than At ₹255 today: → P/E: 8.6x on 79% profit growth → P/B: 0.83x (below book value of ₹283) → Promoter buying at these levels If ROE stays above 15% for 4 quarters without dilution, re-rating from 0.9x to even 1.4x book is 55% upside. To 1.5x book (still half of CreditAccess) is 80%. Risks. → Microfinance is inherently volatile. Political interference at ground level is real → North India concentration still exists → No strategic investor = permanently higher cost of borrowing vs peers → Could remain a value trap if credit cycle turns again ━━━━━━━━━━━━━━━━━━━━ But 0.83x book. 79% PAT growth. Promoter putting ₹100 Cr in. A man who has bet everything on this company twice and won both times. The market prices pedigree. HP Singh does not have it. But fundamentals eventually win. Not advice. DYOR. But when a founder is telling you with his own ₹100 Cr at below book value, that is a signal worth studying. 🔥 Save this. Come back after Q1FY27 results.

@malpani Markets have a very short memory. When the momentum continues and the stock starts marching towards ₹1,200 -1400 the same people criticizing today will start calling Gautam Singhania the next Niranjan Hiranandani.

@kenneth030394 Human Emotions take over rational thinking on both Upside and Downside.

Funny how the stock market works. When a stock is available at throwaway valuations, everyone has 100 reasons why it's cheap for a reason. When it starts moving, it's called a trap. After it goes 2–3x, everyone suddenly wants to own it. Near the top, people create narratives to justify any valuation. Then the stock falls... and they become long-term investors. The cycle repeats every single time. 📈📉

Just look at DLF. People are willing to pay a huge premium for the brand. Apartments at The Camellias and The Dahlias have sold for well over ₹100 crore, showing the kind of pricing power a trusted brand can command. Raymond Realty may be a much smaller player, but its track record of delivering projects ahead of schedule could become a major competitive advantage. Over time, that credibility should help it win more redevelopment projects across the MMR region.

@SouvikG1982 Company is professionally managed nothing much to worry.

Raghav Rathi @raghavrathi27

345 Followers 828 Following Not a Registered Investment Advisor, Broker/Dealer,Financial Analyst.View expressed r purely for study purpose.RT not verified. Keep learning & growing together

Equanimity2010 @equanimity2010

191 Followers 2K Following

Vishnu Agrawal @vishnu_vikal

0 Followers 4 Following

Vijaya Suresh @CAVijayaSuresh

374 Followers 1K Following Proud to be an Indian | Passionate about Hindu Scriptures- Indian History - Folklore & CarnaticMusic

Aayush Maurya @aayushhhmaurya

11 Followers 303 Following

vishnu @bluecheran

163 Followers 5K Following

Ritesh @Ritesh84986124

7 Followers 51 Following Software Developer | IIT BHU Grad Technology, Markets, Equities & Continuous Learning

Raj Chatterjee @rajbond123

47 Followers 438 Following

P.D.Sundar @pdsundar1

3 Followers 454 Following

EQUITY EMPIRE 💰 @Ishan_Narayan_

12K Followers 489 Following 21 | ACCA | NISM | SMALL & MICROCAPS | MUTUAL FUNDS | BONDS | Passionate about Financial Freedom | NOT SEBI-REGISTERED | Tweets are not recommendations

Vinod @HassijaVinod

136 Followers 7K Following

subramaniam konar @subramania28533

7 Followers 373 Following

Anil Kewalramani @anilkewalramani

54 Followers 962 Following

Ram @ramkarthikeyan

35 Followers 450 Following

Manan Jain0708 @MananJa54391418

32 Followers 497 Following just a kid who has some pretty big dreams💫

Sanyam Jain @sanyamjain____

0 Followers 10 Following

Joyjit Goswami @goswami_joyjit

5 Followers 61 Following

Vasanth Kumar @ConnectVasanth

60 Followers 314 Following Industrial Commodities Pricing Professional

Nisha Shah @Nisha0182

11 Followers 482 Following

Deepak Agarwal @deepak_agarwal

84 Followers 533 Following

Rishi Jayswal @the_velvet_ug

5 Followers 62 Following

Kaustubh Yeole @KaustubhYeole

4K Followers 119 Following Equity Research Analyst | Sharing Stock Market Insights, Deep Research & High-Conviction Ideas 💹 Not SEBI Registered

gautam peswani @drgautam18

121 Followers 3K Following

Parveen Dhanda @parv43317

6 Followers 104 Following

Sagar @rand0mwalkman

119 Followers 640 Following Topics: Finance | Science | History Background: Trader | ex-Deutsche Bank | IIT Delhi | ESCP

CA Vignesh Baliga @vigz_baliga

15 Followers 300 Following

Amit Agarwal @_Amit_Agarwal_

37 Followers 89 Following

RoB @FinverseNow

1 Followers 10 Following

Abhilash Varghese @webmailabhi

47 Followers 169 Following

Uday Somaiya @UdaySomaiy45051

15 Followers 167 Following

Ankit @acaankitc

129 Followers 1K Following Chartered Accountant by profession.passionate about learning in life.

pooja doshi @poojadoshi817

26 Followers 340 Following

Dr.Pratik Pravin Dosh... @secclue

83 Followers 280 Following Bharatiya | Plant Protection | Sustainable Agriculture | IPM | Scientist

venkata ramana @venkataramana5

308 Followers 3K Following

Dilip @dilipkumarshaw

184 Followers 1K Following

Niran Chengappa @Chengappa_N1980

2 Followers 14 Following

raj @rajkumarnalluri

6 Followers 177 Following

Vijay Tiwary @vijayk_tiwary

13 Followers 170 Following

Saurabh Chhikara 🇮... @SaurabhChhikara

904 Followers 1K Following Observer of mega trends | 3rd generation former Army officer l Wedded to the soil l Views are personal I RTs ≠ Endorsements #LivingTheExponentialAge

Yugandhar @Yugandh45108105

3 Followers 98 Following

Ramesh Shahapurkar @RameshShahapur3

2 Followers 70 Following

Naveen GD @gdnaveen

62 Followers 1K Following

Satish Patnaik @patnaiksatish84

4K Followers 92 Following Breathe Equities - MicroCaps | Ex - Leadership Roles in JP Morgan, EY, Infosys | IIM - Lucknow | KV School |

Harley XVI (finwizz.l... @xvi_harley

11K Followers 131 Following IIT Delhi 2016 | Finance | Stock analyst Founder @ https://t.co/YHd2U98df4 ONLY PLATFORM IN INDIA giving 12 month orderbook, fundraise, concall for all listed 6000+ stocks

Samisosa @samisosa1234

9K Followers 523 Following FOOLISH INVESTOR| I'm DUMB so by default please assume nothing is a BUY / SELL Advice. No Whatsapp/Telegram Groups,No courses, Not worth a single rupee of urs

Anbu @AnbuPalani8

10K Followers 953 Following Thiagarajan Kumararaja Fan || IIM Mumbai || My investment journal || concentrated portfolio

Plutus Advisors @plutusadvisors

15K Followers 7 Following SEBI Registered Research Analyst | Known for FTDB Model | Plutus Advisors – Official Links: https://t.co/aMqnhVZATZ

Saurabh Koratkar @saurabhkoratkar

11K Followers 247 Following Journalist | Criticizer | Investment learner | Experimental chef | News Anchor @zee24taasnews | Ex.TV9 Marathi,Abp majha (Views are personal)

Ashish Kumar Meher @AshishMeher7

19K Followers 3K Following Proud Navodayan | Agriculturist | Algo Trader | Small Cap Investor | NISM Certified RA at Vighnahara Investment | DM for Collab

sandip sabharwal @sandipsabharwal

128K Followers 75 Following RESEARCH ANALYST EQUITY INVESTING INH000008109 IIT Delhi & IIM Bangalore Ex Head of Equity SBI MF, CIO JM Financial Stock Market Investing

Parth Goyal @StocksRoyale1

15K Followers 180 Following I live & breathe markets | Research Analyst @NDTVProfitIndia

Volatility Volume and... @VVVStockAnalyst

126K Followers 24 Following IIT Madras | Building @ValvoIntel | 8 Figure Momentum Trader | Quantitative Market Researcher

Aakash Jha @AakashJha_AJ

3K Followers 142 Following Investor | Equity Analysis | Business Research. Views are personal and are not recommendations.

Normal Guy @Normal_2610

21K Followers 972 Following Investor | policy | politics | Geopolitics | Defence | AI | Observer & Commentator | Critic | stay curious वीर भोग्या वसुंधरा

Manish Khandelwal @ManishK46113331

25K Followers 3K Following Investing 🕵️♂️ | Geo-politics 🌍 | Football ⚽ | Coding 👨💻 | Running 🏃♂️| Views are personal

Cryptified Soul (Gari... @Cryptified_Soul

30K Followers 637 Following 💓Stocks | 🚀Tech and Fundamental Analysis | 👁Views are personal | 🛠Managing my own PF | 🛣Long Term | 📈Equities | SEBI Unregistered | DM for collab

SIP Investor @SIP_INVEST0R

11K Followers 830 Following SIP is the easiest way towards long term wealth creation. Just SIP in a handful MFs and quality stocks regularly for long to see the wonder!

A Microcap Investor @amicroinvestor

14K Followers 1K Following ▪️Long Term Investor ▪️BigBull on India ▪️Biased towards Value than Growth ▪️Personal Views ▪️No Recommendations

Aditya Shah @AdityaD_Shah

135K Followers 597 Following Founder Hercules Advisors-Stocks,Financial Planning,Insurance and Mutual funds DM us for enquiries, or email at [email protected]

@Equity_Explorer @roy_udit43139

810 Followers 2K Following Equity Explorer | Stocks • MFs • ETFs | | Views are personal I Not SEBI registered l Virat Kohli Fan I Cricket & Football Lover I

Manish K @manish21688

402 Followers 125 Following Technology Professional. On a mission to 3X my corpus by 2030 by blending signals from macro and micro and leveraging AI

Finding multibaggers ... @TheFitNiveshak

1K Followers 867 Following •Investor | TechnoFunda •Helping investors catch earnings-surprise stocks early •Get my Premium Strategy

RonnieV @TheRonnieVShow

65K Followers 260 Following Momentum trader | Growth investor Founder @ValueSnapshotio ↓ Research • Trades • Investing • Tools ↓

Darvas Box Trader @darvasboxtrader

112K Followers 46 Following Trend Rider. Patience 100% 🚫 Not SEBI Registered *Financial Tweets are for my learning purpose only *

Shashi Sachan @Sachan8574

11K Followers 2K Following @Option seller!! 7+ yrs in markets From losses → consistency Sharing what actually works DM ‘LEARN’ — https://t.co/UupuzttxHp

Sanchit Narula @narula_san60939

4 Followers 85 Following

Amitabha Dash @AmitabhaDash

2K Followers 2K Following Long-term investor | 16 yrs equity journey | Stocks • Mutual Funds • ETFs • Working in IT industry | Personal views | Not investment advice

LNPR Capital @LnprCapital

39K Followers 61 Following We don’t chase multibaggers. We build conviction before they’re called multibaggers. SEBI registered RA : INH000012953

Market Avenues @MarketAvenues

5K Followers 650 Following Indian Equity Markets | Nifty | BankNifty | Stocks Mutual Funds | SIPs | Investing | Chart Analysis Educational Purposes Only | Not SEBI Registered

BRICS News @BRICSinfo

2.1M Followers 2 Following We are an independent media company bringing you unparalleled coverage of all-things geopolitics & BRICS News in real-time. Not an official government account.

Sadaf Sayeed 🇮🇳 @Sadafsayeed

6K Followers 2K Following CEO @MuthootMicrofin #Entrepreneur #Investor #Mentor #VC #FinancialInclusion #Digitalinclusion #InclusiveGrowth

Ginger Investor @GingerInvest44

12K Followers 2K Following Trader & Investor 🎯🚀, Stock Analysis 😍, Investing theories⌛, Daily trade analysis 💹, Not SEBI registered ❌. No reco ❗. Views are personal 👋

Laysono @Laysono5

973 Followers 1K Following Foot, Barça 🟦🟥, mangas et animés mes passions du quotidien Ici pour discuter tranquillement et partager mes délires

Abhishek Gulati @Abhishek25glt

3K Followers 466 Following Stock Market | Fundamental + Technical + Psychology | Spirituality | No Recommendation - P. Views

منصیفہ۔ @aisajut1

5K Followers 5K Following ✨ Turning dreams into reality, one step at a time. 🔥 Hustle, passion, and positive vibes only.

Ritu Agarwal @CA__Ritu

313 Followers 464 Following 💼Chartered Accountant | Public speaking | Entrepreneur | Health freak | Passionate Investor | Reach out for Tax filings

Darshit Patel @darshitpatel84

180K Followers 116 Following Founder @equitynest2022 | AMFI Registered Mutual Fund Distributor ARN- 355670 | 20 Years+ in to Wealth Mgmt | “Stock Market is Mahabharat-Be your own Krishna”

Shivaji Vitthalrao�... @shivaji_1983

115K Followers 62 Following Engineer turned Fund Manager. Founder/CEO Samarth Wealth Management, Managing 3 Funds | @Samarth_wealth|Ex-Valeo-Siemens|Ex-Honeywell|Ex-HCLTech|Ex-Bosch|Ex-ADA

DarvaX Trader 🔆 @AmitabhJha3

230K Followers 259 Following Captain Navy .Ramta Jogi . Happy DarvaXian 🔆 Tweets for Educational Purpose only SEBI Unregistered

Rishikesh Singh @Rishikesh_ADX

342K Followers 90 Following Co-Founder of InVed® Equity4Life® | Investor | Trader | Mentor. SEBI RA: INH000012351 (Partner) Equity4Life IH Analytics Pvt Ltd.

Nikita Poojary @niki_poojary

169K Followers 96 Following Tweets and threads about Price Action, Trading Strategies, Option Selling & Psychology. https://t.co/roUM2NVQcm

Aditya Todmal @AdityaTodmal

199K Followers 83 Following 29 | Option Writer | Expiry Trader | Avid Reader | Tweets and threads about Price action Option Selling & Trading growth.

Pankaj Parekh @DhanValue

147K Followers 13 Following Avid Reader | Data-Driven Research & Analysis | SEBI Unregistered | Let Data Speak Louder Than Words | Sharing insights freely for better investing.

Investing @ Prakash @Prakashplutus

217K Followers 116 Following Founder - Plutus Advisors | SEBI Registered Research Analyst - Plutus Advisors | Investor 18+ Years of Exp. |

jeevan patwa @jeevanpatwa

55K Followers 4 Following CIO, Sahasrar capital private limited (PMS - SEBI REGN No INP000007386), CFA, MTech (IITK) All tweets are for educational purpose. No reco

The Disciplined Inves... @Disciplined_Inv

29K Followers 335 Following Disciplined Value Investor | IIT KGP Alumnus, CFA Level 3 Cleared | Not SEBI registered.

Rohit D Kriplani @rdkriplani

29K Followers 362 Following I share my equity journey mixing fundamentals + technicals + human behaviour. SEBI Registered RA - INH000021298.Trends for United States

You might like