Flash by StockSentinel.ai @SentinelFlash

Elevate your investment strategy—Flash's AI podcasts and reports give you new ways to uncover the best investments in a flash. 100% FREE Reports! flash.stocksentinel.ai Joined December 2024-

Tweets18K

-

Followers2K

-

Following62

-

Likes4

PrairieSky Royalty Ltd. $PSK.TO operates as a premier energy landlord in Canada, controlling a massive and perpetual fee simple mineral title land package across the prolific Western Canadian Sedimentary Basin. By licensing subsurface rights to third-party operators who cover all capital and environmental costs, the company achieves near-perfect cash flow conversion and operating margins of roughly ninety-eight percent. While standard producers trade at much lower multiples due to heavy reinvestment needs, this low-risk business model commands a premium valuation supported by organic growth catalysts like rapid multilateral drilling in the Clearwater and Duvernay plays. This structural cost insulation and disciplined capital allocation have allowed management to aggressively pay down debt and return capital directly to shareholders through consistent share buybacks and dividends. Will other energy sector players find a way to replicate this high-margin landlord model, or will PrairieSky continue to dominate as the ultimate defensive compounder in Canadian oil and gas?

Most investors avoid $PSK because it trades at 18x cash flow while typical oil and gas stocks sit at 5x. But they are missing a crucial structural distinction: this company has a 98% operating margin, zero capital expenditures, and zero environmental liabilities. It is not an energy producer; it is a perpetual subsurface landlord. Here is why the apparent valuation premium is actually a massive market misunderstanding. #EnergyInvesting auth.flash.stocksentinel.ai/functions/v1/v…

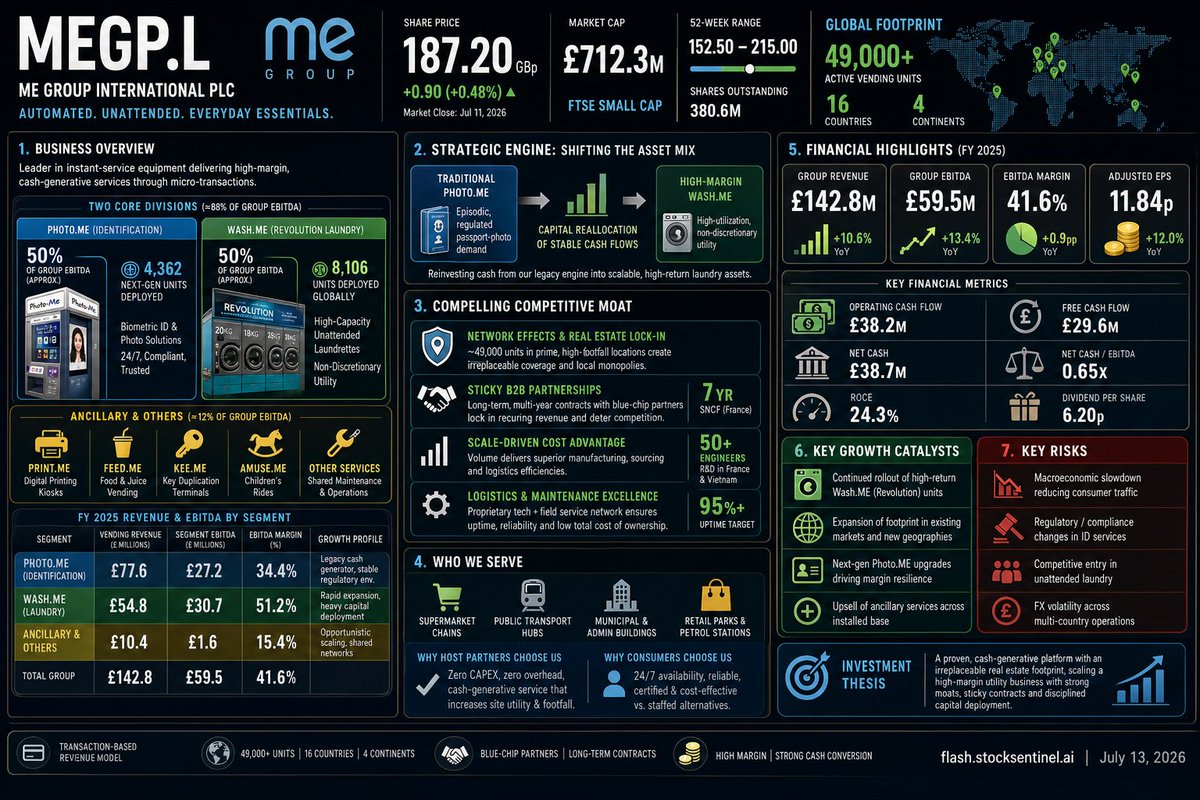

ME Group International plc $MEGP is transforming its business model by transitionally shifting from legacy photo booths to high-margin unattended laundry stations. The company currently trades at an exceptionally low trailing price-to-earnings multiple of just under seven times, which is highly disconnected from its strong return on capital metrics. With more than forty-nine thousand active units operating globally, this business utilizes its legacy cash flows to entirely self-fund a rapid international rollout program. Despite a recent temporary slowdown in consumer spending in France, trading has rebounded robustly, and major brokers continue to reiterate highly optimistic buy ratings. Will the ongoing global expansion of laundry units successfully drive a comprehensive valuation re-rating for this deeply discounted compounder?

The market still prices $MEGP like a dying, paper-passport photo business at a TTM P/E of just 6.9x. What they are completely missing is a massive, self-funded pivot into automated outdoor laundry, which now drives over 54% of EBITDA at a stunning 51% margin. This is a high-utility compounder with a 31% ROCE hiding in plain sight. Here is our deep dive into the ultimate asymmetric small-cap. 📊 #ValueInvesting auth.flash.stocksentinel.ai/functions/v1/v…

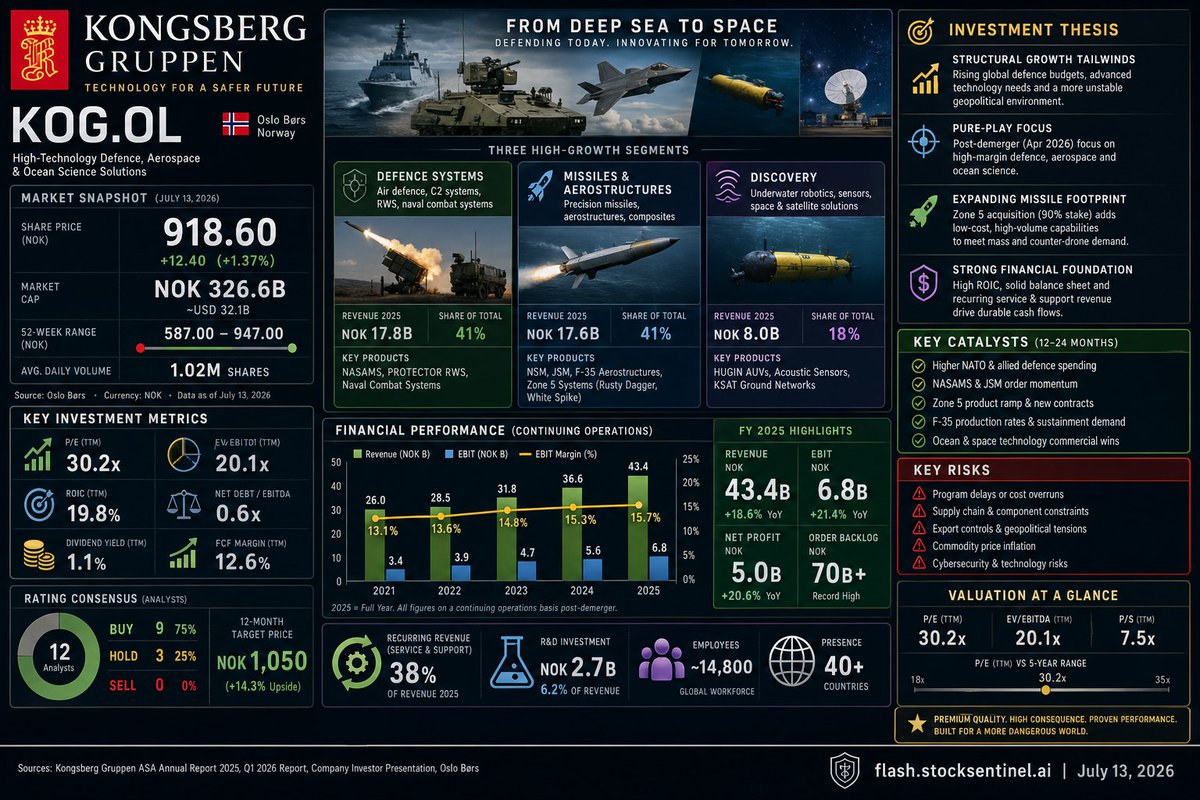

Kongsberg Gruppen ASA $KOGO.OL has successfully positioned itself as a premier European defense and aerospace technology pure-play following the strategic spin-off of its civilian maritime operations. Backed by a historic order backlog of over one hundred and fifty-seven billion Norwegian kroner, the group is rapidly scaling its manufacturing footprint across Poland, Australia, and the United States to meet soaring global demand for advanced air defense and stealth missile systems. However, the stock currently trades at a premium trailing price-to-earnings ratio of over fifty-five times, reflecting high market expectations that leave little room for execution delays or supply chain bottlenecks. While some institutional analysts caution against this elevated valuation, others argue that the multi-decade tailwinds from NATO spending commitments will drive sustained long-term growth. Can this specialized niche leader expand its global production quickly enough to justify its premium stock price and fulfill its massive backlog?

The market just dumped one of Europe's premier defense technology compounders over a simple paperwork delay. While consensus panics over a temporary dip in cash, the reality of $KOGO.OL is a massive NOK 157B backlog and a business that just broke quarterly revenue records. Here is why today's 5% sell-off is a textbook valuation disconnect—and where the stock goes next. 🎯 auth.flash.stocksentinel.ai/functions/v1/v…

Grupo Aeromexico $AERO operates as Mexico's sole full-service global carrier, commanding a robust economic moat through strategic wide-body exclusivity and key slot scarcity at its Mexico City hub. Although near-term profits are temporarily squeezed by high jet fuel prices and currency-driven wage inflation, the company maintains a highly resilient financial core supported by 1.2 billion dollars in total liquidity. Forward-looking investors are closely watching a compelling valuation gap, as the stock trades at a steep discount to its global peers at approximately 3.5 times projected 2027 enterprise value to EBITDAR. Long-term business prospects remain anchored by the ongoing legal protection of its joint venture with Delta Air Lines and management's active commercial strategies to fully recover incremental fuel costs by the fourth quarter of 2026. Will this premium airline successfully navigate its short-term cost headwinds and low-cost domestic competition to unlock its massive projected valuation upside for patient shareholders?

While the market obsessively prices in short-term fuel spikes, they are practically giving away Mexico’s only wide-body international carrier at a steep 3.5x forward multiple. With a critical earnings catalyst dropping after the bell today, we break down why institutional money is quietly positioning in $AERO while retail traders stare at the rearview mirror. ✈️ #ValueInvesting auth.flash.stocksentinel.ai/functions/v1/v…

Kongsberg Gruppen ASA $KOG.OL has successfully positioned itself as a pure-play defence, aerospace, and ocean science leader following the strategic demerger of its maritime business. The company is experiencing unprecedented demand, resulting in a record-breaking order backlog of NOK 158 billion that provides high revenue visibility. While the stock currently trades at a valuation premium compared to traditional defense peers, this premium is backed by superior cash flows and the acquisition of US-based Zone 5 Technologies. With ambitious long-term goals to triple revenues to NOK 100 billion by 2029, the group remains a critical sovereign partner in a highly fragmented geopolitical climate. Will the company overcome near-term supply chain and labor constraints to fully capitalize on this historic defense spending supercycle?

The market just sold off $KOG over a minor margin miss, completely missing the bigger picture. This Norwegian defense giant is sitting on a record NOK 158 billion backlog with plans to triple revenue by 2029. The bottleneck isn't order demand—it's how fast they can scale production. Here is why this technical pullback is a major gift. 🎯 auth.flash.stocksentinel.ai/functions/v1/v…

Aya Gold & Silver Inc. $AYA is a Canadian-headquartered precious metals miner operating the flagship Zgounder Silver Mine in Morocco as a rare primary silver producer. The company recently reported stellar financial results for the first quarter of 2026, with revenues skyrocketing 247% year-over-year to $117.27 million and gross profit margins expanding to 71.5%. Backed by a record Q2-2026 operational update that saw consolidated production surge 61% year-over-year, management is confidently targeting an aggressive scaling of annual output to 43 million ounces by 2029. With a trailing P/E of just 13.36x reflecting a discount to its multi-billion dollar Boumadine project pipeline, can this low-cost operator successfully execute its growth roadmap to deliver massive returns for investors?

The market panicked over temporary winter weather bottlenecks, missing the real story. While Wall Street focused on Q1 EPS noise, $AYA quietly cleared the runway—posting a massive 61% YoY production surge in Q2. At a 13x trailing P/E, this rare primary silver producer is self-funding an 8x output expansion by 2029. Here is the contrarian catalyst the market is pricing at zero. ⚡ #Silver auth.flash.stocksentinel.ai/functions/v1/v…

GoGold Resources Inc. $GGD is transitioning from a single-asset tailings processor into a mid-tier precious metals producer by developing its flagship Los Ricos South project in Mexico. The company boasts an exceptionally robust balance sheet with two hundred eighty-four million dollars in cash and zero debt, enabling it to fully fund its construction plans without dilutive equity raises. This development is supported by its operating Parral Tailings facility, which recently generated a record quarterly operating cash flow of over twenty-one million dollars. While trading at a premium valuation compared to its industry peers, the company is backed by robust project economics and a highly experienced management team with a proven track record. Can this uniquely self-funded explorer successfully navigate Mexico's evolving regulatory environment to unlock its full district-scale potential?

While the market reacted to a technical "revenue miss" caused by shifting gold-to-silver ratios, they missed the real signal. $GGD is sitting on a $284 million cash fortress with zero debt—fully funding a massive silver district with zero dilution. While peers dilute to build in a high-interest rate environment, this outlier is quietly transitioning into a major mid-tier producer. Here is the contrarian thesis. #Silver auth.flash.stocksentinel.ai/functions/v1/v…

Liberty Gold Corp $LGD is rapidly de-risking its flagship Black Pine project, which stands as the largest un-permitted, single-asset oxide gold deposit in the premier mining jurisdiction of Idaho. Backed by a strong, debt-free balance sheet and funded to a final construction decision through non-core asset sales, the company avoids the heavy dilution typically faced by junior developers. Its highly oxidized deposit allows for straightforward, low-cost open-pit heap leaching that bypasses expensive crushing circuits and delivers exceptional metallurgical recovery rates. Trading at a massive discount to its net asset value at current spot gold prices, this project represents exceptional leverage and a highly attractive target for senior producers seeking safe, long-life domestic production. Will Liberty Gold successfully navigate the federal environmental review to achieve first production by 2028, or will strategic interest trigger a premium takeover first?

Junior gold developers are typically written off as dilution traps, but the market is completely missing this exception. Fully funded to construction through non-core asset sales, they own the Great Basin's largest independent oxide gold deposit. At spot prices, $LGD.TO trades at a steep 0.28x P/NAV discount, making it the ultimate premium takeout target. auth.flash.stocksentinel.ai/functions/v1/v…

ILPRA S.p.A. $ILP This precision engineering leader specializes in advanced automated packaging machinery operating at the vital intersection of food preservation and industrial automation. The company posted record net sales of 84 million euros in 2025, representing an impressive 20.2% year-over-year growth rate anchored by strong global exports. Despite achieving an exceptional return on equity of 24.73%, the stock trades at an appealing discount of just 7.0x EV/EBITDA. Its dual-revenue model establishes a sticky installed base that yields highly lucrative, recurring downstream revenues from specialized technical support and packaging consumables. Can this structurally undervalued compounding machinery specialist continue to outperform its larger global competitors as industrial automation demand accelerates?

Most investors ignore industrial packaging as a boring, low-growth sector. They are missing $ILP which has quietly delivered an 18% revenue CAGR and a stellar 24% ROE, while trading at a 40% discount to its peers. This is a high-margin, razor-and-blade compounder hiding in plain sight. Here is the contrarian thesis on why institutional smart money is moving in. auth.flash.stocksentinel.ai/functions/v1/v…

FTAI Aviation Ltd $FTAI is capturing market share in the commercial jet engine aftermarket by bypassing slow, traditional maintenance overhauls in favor of rapid modular engine swaps. This unique model drove a sixty-five percent year-over-year revenue surge to over eight hundred and thirty million dollars in the first quarter of 2026. Although the stock trades at a premium forward price-to-earnings multiple of approximately thirty-three times, this is supported by its profitable transition to a capital-light, fee-earning services structure. Looking ahead, its upcoming launch of industrial turbines utilizing retired engine cores could open up a lucrative new growth segment in the data center backup market. Can this fast-growing aviation platform successfully scale its modular maintenance model and enter the data center power market to justify its premium valuation over the next five years?

Most investors price $FTAI as a cyclical aviation lessor, missing the structural moat of its proprietary parts monopoly. But the real asymmetric edge lies in the ground: they are quietly prepping to launch retired jet engines as backup power turbines for AI data centers. Here is why the street is underwriting the wrong narrative. ✈️ #ValueInvesting auth.flash.stocksentinel.ai/functions/v1/v…

Sylvia @ScriptorEarwig

341 Followers 3K Following When shopping, the cheapest items will be on the top and bottom shelves; not eye level.

CrystalS @steelcompass

634 Followers 854 Following I think I’ve curated my follows to get something useful out of this platform.

volkan alçı @volkanal486150

44 Followers 2K Following

MP @Panmikejr

309 Followers 3K Following

DrJcM @mader_jc

110 Followers 968 Following Medicine & healthcare. Following world economics and investment trends. Nature photographer.

Aphichai_exat @Aphichaich

148 Followers 2K Following

tonyyu2008 @ksyuaa

96 Followers 824 Following

ماس ؟ @csmas2

86 Followers 927 Following

Venkateswarlu Kotte @venkykotte

64 Followers 139 Following

ricardo @ricardofantonio

59 Followers 61 Following

sez_me_man @sez_me_man

5K Followers 7K Following Systems engineer, metals mining investor. Tweet about history, 20th century events, tech, music, pop culture. Advocate US constitutional rights, golden rule.

Fear Not, For I am wi... @Algoholics_anon

1K Followers 5K Following

PM @pedronvmartins

426 Followers 5K Following

Veeresh CK @captveeresh

253 Followers 202 Following

Pankit Shah @shahpankit91

18 Followers 618 Following

Priscilla @g_priscilla99

54 Followers 2K Following i’m not perfect, but i promise i’m fun to be around

TEJAS SHAH @TEJASSH19619270

67 Followers 1K Following

Christina @christinamcelha

356 Followers 4K Following welcome to the naughty corner of the web! where fun never gets old, literally! 😁

Maureen Cunningham @MaureenniRocky

2K Followers 4K Following

karmacomaz @Jvaisldire

4 Followers 89 Following

Cal Little @callitttle

472 Followers 2K Following

Sateesh Reddy @NaredlaSateesh

295 Followers 5K Following

Politickr @Politickr

929 Followers 5K Following Politics, predictions, political prediction markets, puns, pasta, and media law

Víctor @melasdas1

152 Followers 906 Following

Nitin Mudaliar @Iceman29081623

40 Followers 222 Following

Briscoe2 @briscoe224

203 Followers 1K Following

Margerita Radabush @TrickeyErin

44 Followers 214 Following

tapebrief @tapebrief

20 Followers 40 Following Analyst-grade earnings briefs from public sources. Cross-quarter narratives, watch-list-answers, disclosure-quality tracking. 25 names → S&P 500.

Rick @Reed77777

1 Followers 47 Following

Torque & Trends @ek1uno

288 Followers 547 Following

Bananas🍌🍌🍌 @GiganticBananas

512 Followers 878 Following Hobby investor trying to be wrong less often 🍌

Werner M. Fait @wernairfight94

372 Followers 370 Following

Dean Robert T. Zaide @t_zaide

4 Followers 45 Following

☔ Defi @UmbrellaDefi

768 Followers 1K Following

Mary @Mary96274267086

34 Followers 2K Following new 2 this whole thing 🌱 constructive criticism only pls

desti torres @DestiT79780

35 Followers 180 Following

Emanuele Pani @66Emanuele66

165 Followers 743 Following

Jambo @PinotNoirRocks

161 Followers 149 Following Lover of Pinot Noir and St Laurent from everywhere

Michael Morgan @thajuice100MM

80 Followers 303 Following

Sam Badawi @Sam_Badawi

51K Followers 624 Following Livestreams & deep dives on stocks, fundamentals & Solid Talk | Stock Talk Insiders, use code "SAM" for 10% off, link below ⤵️

Gene Munster @munster_gene

99K Followers 141 Following Managing Partner @deepwatermgmt. Investing in tech-driven growth. All views/opinions are personal and not investment advice. 🚀

総合商社マン @sogoshoshaman

99K Followers 1K Following 現役商社マン(5大のどこか)🏢社内のモブ🏃個人投資家💰愛妻家&愛犬家🐶子育て中👨日本株🇯🇵米国株🇺🇸世界株🌏暗号資産BTC HODL✊「投資は楽しく!」がモットー😘30代で純金融資産2億円達成💸26年4月3億円達成🥷ブログ「商社マンは今日も走る」執筆🏃♂️案件相談DMへ📩垢これだけ⚠️

Tahmineh Dehbozorgi @DeTahmineh

34K Followers 3K Following ⚖️ Attorney | 🇺🇸 American Dream Enjoyer | Metalhead | views are mine

Kyle Adams @KyleAdamsStocks

16K Followers 1K Following 30 | Investing to $1,000,000 in my taxable brokerage | Crazy enough to jump out of planes for fun | not financial advice

Dan Ives @DivesTech

300K Followers 393 Following Official account of Dan Ives. Tech analyst on Wall Street for over 25 years. Advisory Board of Zeta 🎯🔥🏆🐂🕶️🌎✈️

zerohedge @zerohedge

3.1M Followers 960 Following

Micro2Macr0 @Micro2Macr0

114K Followers 9K Following Macro Economist - Self-made multimillionaire - Formerly Retired at 42 - Always trying to find companies and investments that are solving tomorrows problems

unusual_whales @unusual_whales

4.6M Followers 2K Following Stocks/Options/Crypto/Market News/Tools. Not advice @Polymarket partner Open a tastytrade account: https://t.co/wGf2ZdlXpw Discord: https://t.co/0xJ9e0ZYYG More: https://t.co/nsxZlPV0pC

Dividendology @dividendology

118K Followers 1K Following Follow for the Best Dividend Growth and High Yield opportunities! 250k subs on YouTube and growing!

Cathie Wood @CathieDWood

2.6M Followers 515 Following Founder, CEO and CIO @ARKinvest. Thematic portfolio manager for disruptive innovation, mom, economist, and women's advocate. Disclosure: https://t.co/chxRD4oWOd

Nancy Pelosi Stock Tr... @pelositracker

1.8M Followers 722 Following Highlighting Politicians' trades so we can invest alongside. $1.7B invested alongside via @joinAutopilot Download Autopilot to trade like a politician

Marcin Michałek @MMichalek91

2K Followers 510 Following White collar miner, mining arbitration commentator and investor, speculator, mining claims investing early adopter, shareholder-activist. $GRX $EML $PAT

Sabine VanderLinden @SabineVdL

50K Followers 25K Following Venture Client Model Architect | CEO Alchemy Crew Ventures | Board Chair | Host #ScoutingforGrowth | Where Fortune 500s meet growth ventures | #Frontier #AI

Kris Patel 🇺🇸 P... @KrisPatel99prvt

2K Followers 945 Following Reserved for discerning trade talks. Engage in comprehensive stock market analysis and in-depth price insights. Only for a few here. MAIN PAGE: @krispatel99

Thomas (Tom) Lee (not... @fundstrat

638K Followers 940 Following CIO Fundstrat Capital @FundstratCap $GRNY $GRNJ| Research Head @fundstratdirect | @CNBC Contributor | Chairman @BitMNR $BMNR BitMine | Wikipedia: https://t.co/8QsXKpzGT7

Sachin Sharma 🇮�... @sachinvats

29K Followers 686 Following Investor | 🇮🇳 living in 🇲🇾 | 22+ yrs in O&G & ENERGY (20+ yrs in SLB & MBB) | (Opinions only | No Financial Advice | Do your own DD | Don't fall for SCAMs)

Just a Dude Who Inves... @DudeWhoInvests

94K Followers 2K Following Investing, Economics, News, Tech, Memes, Shenanigans, & Whatever Is Trending. NOT Financial Advice & Watch Out For Fake Accounts. I Won’t DM You.

Kris Patel 🇺🇸 @KrisPatel99

44K Followers 752 Following If you can overthink the worst, why cant you overthink the best?

Kyle Grieve @IrrationalMrkts

31K Followers 405 Following Host of We Study Billionaires podcast | Empowering retail investors to compound wealth with stocks | '20-'25: 19% Compound Annual Gain

Farzad 🇺🇸 🇮�... @farzyness

385K Followers 2K Following Abundance or Collapse: https://t.co/IZNjdFzcwi Master Plan: https://t.co/Ujh87zX3TJ

Alberto Echevarría |... @MonkEchevarria

10K Followers 396 Following What if a single score told you exactly which stocks deserve your money? I built it. Backtest result? $10K → $1.98M / 25 yrs. Past performance ≠ future returns.

David Carbutt @DavidCarbutt_

11K Followers 287 Following Helping you build a top 1% YouTube channel 📈 100M+ views & $ Millions generated from YouTube for my clients. 📩 DM 'YouTube' to join the waitlist

Palantir Daily @DailyPalantir

48K Followers 38 Following Covering the world of Palantir, (NASDAQ: PLTR) daily.

SoFi Investor Relatio... @SoFiIR

16K Followers 230 Following Official Account of SoFi Investor Relations.

Nikki Rush @nikkirush

391 Followers 2K Following Head of Portfolio Equity Trading and Centralised Risk at Morgan Stanley

@jason @Jason

1.5M Followers 7K Following Host: @twistartups @theallinpod @thisweeknai; I invest in 100 startups a year @launch & @founderuni [email protected] for life

Steven Fiorillo @stevenfiorillo

31K Followers 756 Following 📈 Seeking Alpha Analyst | Co-Host @basispointpod | YouTube: @stevenfiorillo1 | https://t.co/3Z1vDFtXba |TipRanks #12 Financial Blogger & #19 Expert

Mohnish Pabrai @MohnishPabrai

266K Followers 976 Following Pabrai Funds, The Dakshana Foundation, @wagonsetf; author of The Dhandho Investor and Mosaic. Views are my own.

Tom Nash @iamtomnash

184K Followers 3K Following 📈 Investor | Founder of https://t.co/3Zg2kEd1iS | YouTuber 💰 Long-term investing, DCA, & market insights 🇺🇸 $PLTR Early Investor

Donald J. Trump @realDonaldTrump

111.7M Followers 53 Following 45th & 47th President of the United States of America🇺🇸

Tannor Manson @Futurenvesting

50K Followers 487 Following Curious about tech, investing, and where the world’s headed. Subscribe to the Future Investing YT Channel to stay in touch!

Jeremy Lefebvre @HolySmokas

130K Followers 76 Following Stock-picker since 2008, YouTuber (900k subs), flap-jack flipper 🥞 ,husband and dad. I make $ into more $ you can LEARN it, too! 💸 @HolySmokas my ONLY account

Brian Feroldi @BrianFeroldi

668K Followers 517 Following 🔎 I Teach Investors How To Analyze Businesses | Author & Financial Educator | 20+ Years Investing Experience | Building Stock Simplifier ⬇️

Daniel Mahncke @MnkeDaniel

119K Followers 247 Following For Weekly Company Deep Dives, Subscribe to the Free Intrinsic Value Newsletter: https://t.co/LxBKfdsrlg

Admiral Risky @AdmiralRisky

1K Followers 439 Following Whenever there is fear, there is opportunity. Investing | Technology | Data

Special Situation Inv... @SSI_invest

58K Followers 441 Following Event-driven trades and low risk arbitrage opportunities with short term catalysts. Merger Arbitrage Tracker.

Morningstar, Inc. @MorningstarInc

239K Followers 684 Following We are a leading provider of independent investment research. Our mission is to empower investor success.

Nomad Cat @nomadcat

799 Followers 218 Following Tweeting on investing, startups, entrepreneurship, technology and developing markets

UNRIVALED INVESTING @UnrivaledInvest

8K Followers 967 Following Prior Banker, Hedge Funder & CFO. Investor on YouTube. Looking for exceptional companies & UNRIVALED investments.

National Geographic @NatGeo

27.9M Followers 179 Following Step into wonder and find your inner explorer with National Geographic 🌎

You might like