CompoundingAI @compoundingaiin

Institutional Grade AI Market Research Assistant Login to CompoundingAI Now : https://t.co/A7jTkCcNSz compoundingai.in Joined September 2024-

Tweets6K

-

Followers7K

-

Following43

-

Likes3K

@Stockibull Hey Gitesh, You can check out Turtlemint Q1 FY27 results here. compoundingai.in/share/kyqGoCeR…

We keep adding companies to our watchlist, but rarely have time to track them. With Agentic Chat, ask questions that would take an analyst hours to answer and get answers in minutes. Upload your watchlist to Portfolio Manager & give it a try. Example- compoundingai.in/share/ZfAYlU0q…

@ETNOWlive For JSW Steel in Q1 FY27, total subsidiary contribution swung from −₹33 Cr in Q1 FY26 to +₹1,825 Cr, an ₹1,858 Cr improvement. x.com/compoundingaii…

Login to CompoundingAI to track results live! (Link in Bio) JSW Steel Q1 FY27 Result Analysis Revenue: ₹47,364 Cr | +18.8% YoY (comparable PF, ex-BPSL) Adj. EBITDA: ₹9,373 Cr | +31.9% YoY | margin 19.8% (was 17.8%) PAT to owners: ₹4,651 Cr | +113% YoY Zero exceptional

@REDBOXINDIA For JSW Steel in Q1 FY27, total subsidiary contribution swung from −₹33 Cr in Q1 FY26 to +₹1,825 Cr, an ₹1,858 Cr improvement. x.com/compoundingaii…

Login to CompoundingAI to track results live! (Link in Bio) JSW Steel Q1 FY27 Result Analysis Revenue: ₹47,364 Cr | +18.8% YoY (comparable PF, ex-BPSL) Adj. EBITDA: ₹9,373 Cr | +31.9% YoY | margin 19.8% (was 17.8%) PAT to owners: ₹4,651 Cr | +113% YoY Zero exceptional

@business For JSW Steel in Q1 FY27, total subsidiary contribution swung from −₹33 Cr in Q1 FY26 to +₹1,825 Cr, an ₹1,858 Cr improvement. x.com/compoundingaii…

Login to CompoundingAI to track results live! (Link in Bio) JSW Steel Q1 FY27 Result Analysis Revenue: ₹47,364 Cr | +18.8% YoY (comparable PF, ex-BPSL) Adj. EBITDA: ₹9,373 Cr | +31.9% YoY | margin 19.8% (was 17.8%) PAT to owners: ₹4,651 Cr | +113% YoY Zero exceptional

@CNBCTV18Live @Nigel__DSouza For JSW Steel in Q1 FY27, total subsidiary contribution swung from −₹33 Cr in Q1 FY26 to +₹1,825 Cr, an ₹1,858 Cr improvement. x.com/compoundingaii…

Login to CompoundingAI to track results live! (Link in Bio) JSW Steel Q1 FY27 Result Analysis Revenue: ₹47,364 Cr | +18.8% YoY (comparable PF, ex-BPSL) Adj. EBITDA: ₹9,373 Cr | +31.9% YoY | margin 19.8% (was 17.8%) PAT to owners: ₹4,651 Cr | +113% YoY Zero exceptional

@NDTVProfitIndia @StocksRoyale1 For JSW Steel in Q1 FY27, total subsidiary contribution swung from −₹33 Cr in Q1 FY26 to +₹1,825 Cr, an ₹1,858 Cr improvement. x.com/compoundingaii…

Login to CompoundingAI to track results live! (Link in Bio) JSW Steel Q1 FY27 Result Analysis Revenue: ₹47,364 Cr | +18.8% YoY (comparable PF, ex-BPSL) Adj. EBITDA: ₹9,373 Cr | +31.9% YoY | margin 19.8% (was 17.8%) PAT to owners: ₹4,651 Cr | +113% YoY Zero exceptional

@ZeeBusiness For JSW Steel in Q1 FY27, total subsidiary contribution swung from −₹33 Cr in Q1 FY26 to +₹1,825 Cr, an ₹1,858 Cr improvement. x.com/compoundingaii…

Login to CompoundingAI to track results live! (Link in Bio) JSW Steel Q1 FY27 Result Analysis Revenue: ₹47,364 Cr | +18.8% YoY (comparable PF, ex-BPSL) Adj. EBITDA: ₹9,373 Cr | +31.9% YoY | margin 19.8% (was 17.8%) PAT to owners: ₹4,651 Cr | +113% YoY Zero exceptional

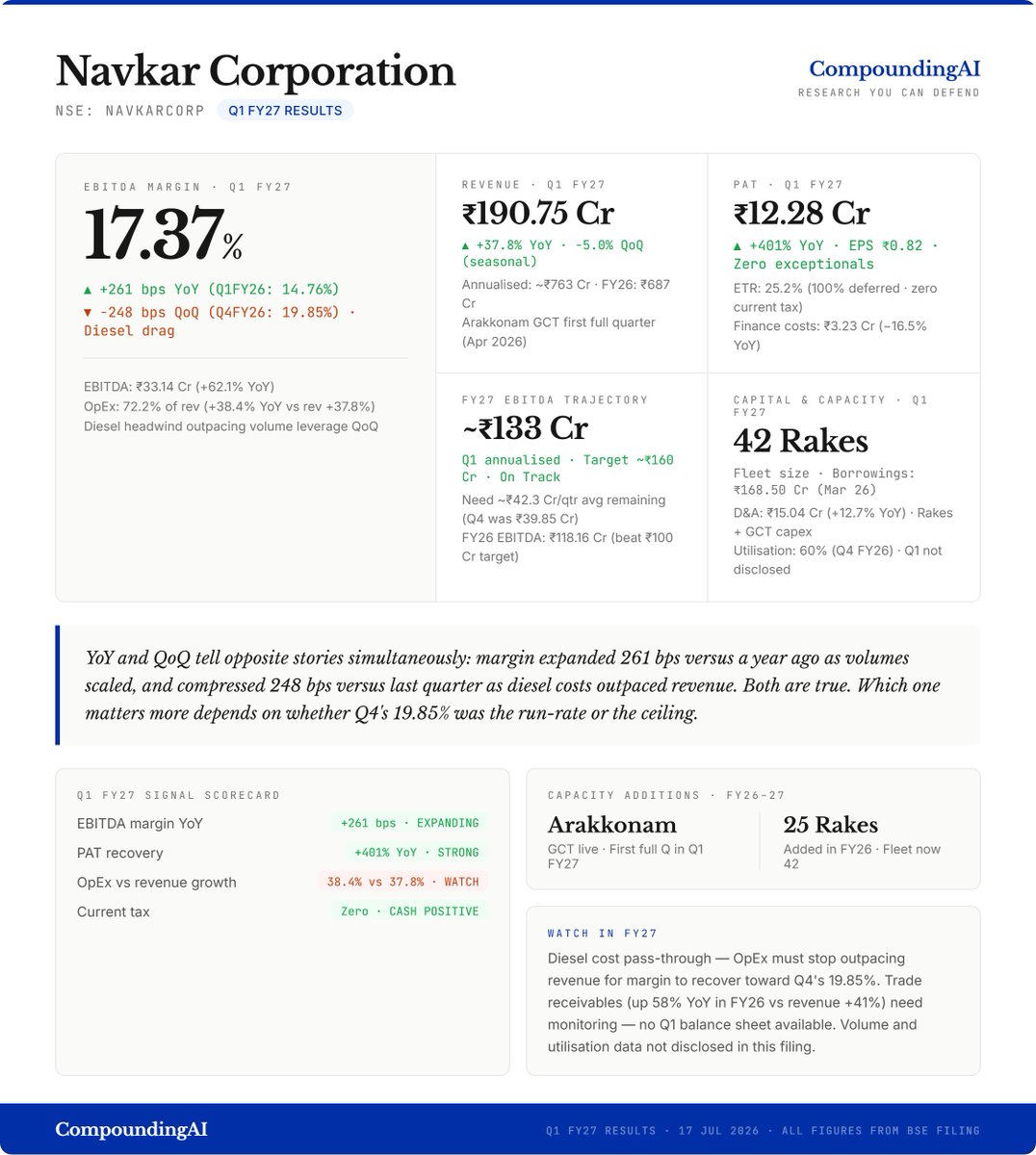

Login to CompoundingAI to track results live! (Link in Bio) Navkar Corporation Q1 FY27 Result Analysis Revenue: ₹190.75 Cr | +37.8% YoY | −5.0% QoQ (seasonal) EBITDA: ₹33.14 Cr | +62.1% YoY | margin 17.37% (was 14.76%) PAT: ₹12.28 Cr | +401% YoY Zero exceptional items. Zero current tax. The 401% PAT growth needs immediate context - the base was ₹2.45 Cr in Q1 FY26, barely breakeven. The real story is whether the margin trajectory is improving or deteriorating. The answer is: both, depending on which direction you look. YoY: EBITDA margin expanded 261 bps from 14.76% to 17.37% - operating leverage from volume growth is real and materialising. Revenue nearly doubled over two years. The Arakkonam GCT terminal (commissioned April 2026) contributed its first full quarter. Fleet of 42 rakes now fully deployed. QoQ: Margin compressed 248 bps from Q4 FY26's 19.85%. Operating expenses grew 38.4% YoY, fractionally outpacing revenue's 37.8%. The culprit is diesel - cumulative hikes of ~₹7.5–8/L through Q1 flowed directly into the operating cost line, which sits at 72.2% of revenue. When your largest cost is fuel, you need volumes to run ahead of price. In Q1 they didn't. The key question is whether Q4 FY26's 19.85% was the run-rate or the ceiling. Management's FY27 EBITDA target implies ~₹160 Cr for the full year. Q1 annualises to ~₹133 Cr - on track, but the remaining three quarters need to average ~₹42.3 Cr against Q1's ₹33.14 Cr. That step-up requires either margin recovery or another leg of volume growth. Finance costs declined 16.5% YoY to ₹3.23 Cr - deleveraging continues. ETR of 25.2% is all deferred tax with zero current tax outflow, a clean cash flow positive. Three things not in this filing: no volume or utilisation data (60% in Q4 FY26, target 80–90%), no balance sheet (trade receivables grew 58% YoY in FY26 vs revenue +41% - that flag remains open), and no update on the Fujairah terminal insurance recovery. Watch: Whether diesel costs stabilise enough for margin to recover toward 19%+. And whether utilisation disclosure returns in subsequent quarters - without it, the quality of the revenue growth is hard to assess. Note: This is not investment advice.

Login to CompoundingAI to track results live! (Link in Bio) JSW Steel Q1 FY27 Result Analysis Revenue: ₹47,364 Cr | +18.8% YoY (comparable PF, ex-BPSL) Adj. EBITDA: ₹9,373 Cr | +31.9% YoY | margin 19.8% (was 17.8%) PAT to owners: ₹4,651 Cr | +113% YoY Zero exceptional items. Net Debt fell ₹7,713 Cr in a single quarter. Note first: BPSL was deconsolidated in March 2026. All comparisons are on a proforma basis otherwise the YoY base isn't comparable. Revenue grew 18.8% but PAT grew 113%. The cause is legitimate: operating leverage plus a collapse in finance costs. Start with margin. Management had guided coking coal up $12–15/tonne. Materials did rise 19.2% QoQ. Adj. EBITDA margin expanded 130 bps QoQ anyway, to 19.8%. Adj. EBITDA per tonne hit ₹14,990 - up 27% YoY. NSR improvement more than absorbed the input cost headwind. That is the most important number in the filing. Finance costs fell 22.8% YoY to ₹1,712 Cr. Interest coverage expanded from 3.78x to 7.08x in a year. This is what structural deleveraging looks like when it flows through the P&L. Balance sheet: Net Debt fell ₹7,713 Cr in one quarter to ₹46,157 Cr, driven by the JFE second tranche of ₹7,875 Cr on June 30. ND/EBITDA at 1.46x vs a ceiling of 3.0x. Both Fitch (BB+ Positive) and CARE (AA+) upgraded in the same fortnight. Subsidiaries were the other driver. JVML Adj. EBITDA surged 138% YoY, delivering ₹1,223 Cr PAT. Coated Products added ₹354 Cr. Total subsidiary contribution swung from −₹33 Cr in Q1 FY26 to +₹1,825 Cr, an ₹1,858 Cr improvement. Capex: ₹4,869 Cr in Q1 against FY27 guidance of ₹22,000–24,000 Cr. BF-3 at Vijayanagar restarted June 23, that 1.5 MTPA increment starts showing in Q2. Sales volumes fell 12% QoQ but that's seasonal; YoY sales grew 4%. Watch: Whether NSR-led margin expansion holds as India turned net importer in May 2026. BF-3 ramp in Q2 is the first clean production read. BMM Ispat amalgamation expected Q4 FY27. Note: This is not investment advice.

Read Havells India Q1 FY27 complete result breakdown compoundingai.in/share/cDAZy3V2…

Login to CompoundingAI to track results live! (Link in Bio) Havells India Q1 FY27 Result Analysis Revenue: ₹6,510 Cr | +19.7% YoY EBITDA: ₹474 Cr | −8.8% YoY | margin 7.3% (was 9.6%) PAT: ₹298 Cr | −15.3% YoY Zero exceptional items. Near debt-free. Revenue grew 20% but EBITDA fell 9%. That's a gap you need to explain before forming a view. One line explains it: A&SP (advertising and sales promotion) doubled from ₹142 Cr to ₹286 Cr - up 100.8% YoY, now 4.4% of revenue vs 2.6% a year ago. That's ₹144 Cr of incremental brand spend in a single quarter. Strip it out and the underlying operating margin is essentially unchanged from Q1FY26. Other SG&A actually improved 100 bps YoY to 8.5% of revenue. The core cost discipline is intact- the question is purely about the A&SP investment call. Which brings you to Lloyd. Lloyd Consumer revenue grew 15.7% YoY to ₹1,460 Cr - the brand is gaining traction. But EBIT losses nearly tripled from -₹20 Cr to -₹51 Cr. The A&SP investment is clearly flowing into Lloyd, which is in an active market-share-building phase in ACs, refrigerators, and washing machines. This is an intentional P&L trade-off. Whether it's the right trade-off depends on whether the market share gains are durable and that won't show in one quarter. Across the Havells segments (ex-Lloyd), every margin compressed YoY. Switchgear at 20.8% (-260 bps), Cables at 10.4% (-220 bps), ECD at 5.2% (-270 bps). Some of this is the A&SP allocation, some is the competitive environment. Renewables is a new standalone SBU - ₹314 Cr revenue (+235.9% YoY, solar/BESS/EV chargers) at a thin 2.7% EBIT as it scales. Cables at ₹2,456 Cr (+27% YoY) remains the largest segment - partly copper price aided, partly volume. Operating cash flow was -₹186 Cr in Q1 driven by working capital absorption (inventory up ₹618 Cr, mainly Cables) and heavy capex of ₹332 Cr. Full-year capex guided at ₹1,400 Cr, primarily for Cable capacity expansion and a new R&D centre. Cash at end of Q1: ₹1,497 Cr. ROE at 18.1% (TTM). Debtor days improved sharply from 16 to 11. Net working capital days down from 43 to 40. Note : This is not an investment advise.

Jio Financial Services Q1 FY27 Concall JIOFIN is scaling to 25M+ app users and AMC AUM at ₹18,412cr. Powered by 16 autonomous AI agents, the platform is driving a daily run rate of ~34,000 product purchases. Read about their transformation in concall- compoundingai.in/share/goJmVLPS…

Jio Financial Services(JIOFIN) Q1 FY27 Concall Income up 141% YoY to ₹1,496cr. Lending AUM hit ₹30,667cr (up 2.6x). Payments hit operational turnaround. With 130 AI agents, they’ve cut credit assessment time by 76%. Read the Q1 concall- compoundingai.in/share/goJmVLPS…

Tech Mahindra(TechM) Q1 FY27 Concall TechM is moving beyond AI hype. With 350+ agents and outcome linked contracts-targeting 40% fewer tickets in healthcare, they are embedding AI into the business core. Read about their transformation in concall: compoundingai.in/share/2AUX39RZ…

Tech Mahindra(TechM) Q1 FY27 Concall Revenue up 6.1% YoY, headcount down 7% YoY. By using AI to boost productivity instead of backfilling, they hit 14.4% EBITDA. Management is rejecting "irrational" industry productivity guarantees. Details in concall: compoundingai.in/share/2AUX39RZ…

Login to CompoundingAI to track live results! (Link in Bio) Alok Industries Q1 FY27 Result Analysis Revenue: ₹993.11 Cr | +6.50% YoY (highest quarterly growth in series) EBITDA: ₹62.48 Cr | 6.29% margin (3.7× QoQ, 2.3× YoY - best in series) Net Loss: −₹138.25 Cr (improved ₹33.31 Cr YoY, ₹54.29 Cr QoQ) Normalised loss (ex-insurance exceptional): −₹155.45 Cr (improved 21.2% YoY) The headline is unambiguously the EBITDA improvement. From ₹16.60 Cr at 1.69% margin in Q4FY26 to ₹62.48 Cr at 6.29% in Q1FY27 - a near 4× sequential jump, the strongest quarterly operating result in the available data. The standalone EBITDA of ₹59.57 Cr per Note 4 of the filing matches the computed figure exactly. Two cost lines drove most of it. Employee costs fell ₹12.84 Cr (-10.16%) YoY as the workforce restructuring absorbed in prior quarters flows through. Power & Fuel fell ₹26.32 Cr (-13.19%) YoY as energy costs moderated from last year's elevated base. Combined, these two tailwinds saved ₹39.16 Cr YoY - nearly all of the EBITDA improvement. One caveat: both are largely base effects from Q1FY26's high costs, not new cost-cutting this quarter. The QoQ trend on Power & Fuel (16.52% → 17.45% of revenue) is actually slightly worsening. The offset: material costs rose 17.92% YoY to ₹538.86 Cr (54.26% of revenue, up 325 bps), reflecting domestic cotton price pressure. This is the active headwind. Now the structural picture. EBITDA of ₹62.48 Cr covers only 41% of quarterly finance costs of ₹150.91 Cr. The company carries ₹17,384 Cr of assigned debt under the resolution plan - this debt is interest-free for 8 years from September 14, 2020. That period ends September 2028. The reported finance costs of ₹150.91 Cr relate to other borrowings. The debt is carried at cost, not fair value, which understates the true economic cost of capital. After finance costs and D&A of ₹66.78 Cr, the company will remain loss-making at current EBITDA levels for the foreseeable future. Exceptional gain of ₹17.20 Cr from an insurance claim settlement for tornado damage to Silvassa spinning plants - same claim that generated ₹25.60 Cr in Q1FY26. One-time, non-recurring. Accumulated losses stand at ₹23,784.41 Cr as of June 30, 2026. Net worth is deeply negative. The going-concern basis is supported by cash-flow projections and the resolution plan framework. Note : This is not an investment advise.

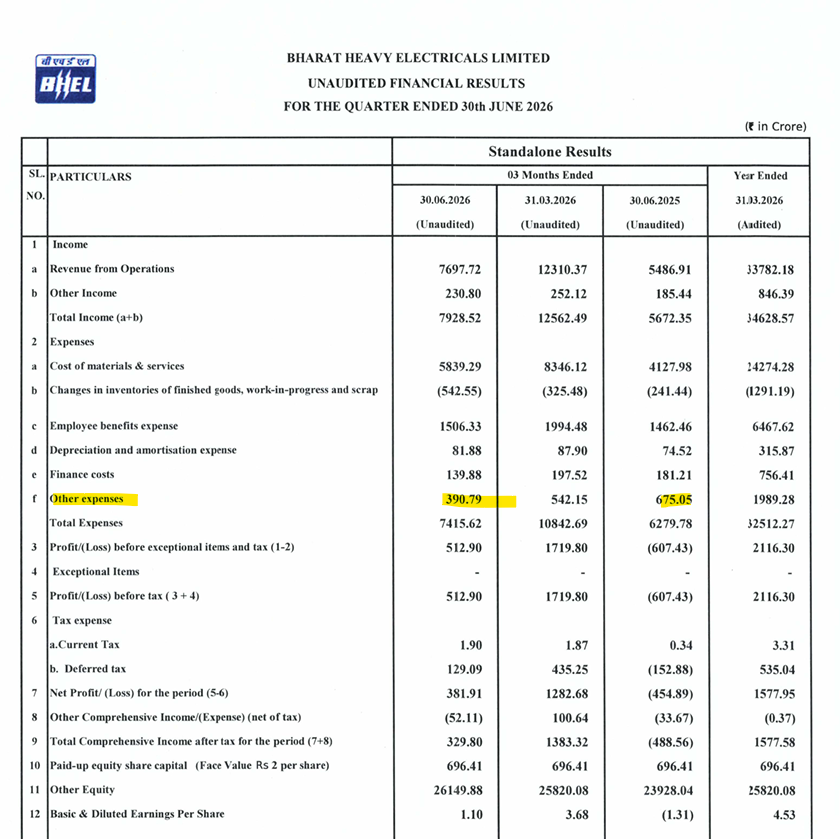

We checked how other expenses have changed in past 12 quarters for BHEL. The 42% drop in other expenses in Q1 FY27 looks like a provision cycle normalisation. The complete conversation here- compoundingai.in/share/ZL--dCl-…

BHEL has seen a big drop in other expenses for the quarter ended 30th June Other expenses at 390 cr vs 675 cr YoY Hence I think need to understand numbers carefully Note - This is not a buy or sell recommendation

@yatinmota Great observation! We checked how this number has changed in past 12 quarters and the 42% drop in other expenses looks like a provision cycle normalisation. The complete conversation here- compoundingai.in/share/ZL--dCl-…

Tech Mahindra Q1 FY27 statement level result breakdown - compoundingai.in/share/3ttTi5u6…

Login to CompoundingAI to track live results! (Link in Bio) Tech Mahindra Q1 FY27 Result Analysis USD revenue: $1,660 Mn | +6.1% YoY | +2.2% QoQ EBIT margin: 14.41% | +59 bps QoQ | +379 bps YoY PAT to owners: ₹1,465.1 Cr | +28.45% YoY | EPS ₹16.53 Zero exceptional items. FCF: $167 Mn (108% of PAT). The headline is the margin. EBIT expanded 59 bps in Q1 - the quarter that always carries the annual salary hike. Employee costs grew only 1.15% QoQ against revenue growth of 4.22%. Unallocable corporate costs fell 57 bps to 6.85% of revenue. IT utilisation rose to 87.0% (+90 bps QoQ). Three levers fired simultaneously, producing the best Q1 EBIT margin in recent history. The 15% FY27 target now needs only ~20 bps per quarter over the remaining three quarters - a pace already exceeded in Q1. USD revenue at +6.1% YoY is the strongest Q1 in years and a clear acceleration from FY26's +1.9% full-year growth. INR revenue of ₹15,711.9 Cr (+17.68% YoY) benefits from the rupee averaging ₹94.6 vs ₹85.3 in Q1FY26 - roughly 6 percentage points of the INR growth is currency, not volume. Look at USD to read the underlying demand. Deal wins of $1,078 Mn mark the third consecutive quarter above $1 Bn. The $50M+ client base expanded from 26 to 33 YoY and from 29 to 33 in a single quarter. Manufacturing was the standout vertical at +17.2% YoY, +9.0% QoQ, directly contradicting the tariff-drag concern. FCF conversion at 108% of PAT is the highest Q1 in the series. DSO improved to 84 days from 95 days a year ago - 11 days of working capital released in four quarters. Net cash position grew to $1,019 Mn from $885 Mn in Q4. Three flags. Other expenses grew 13.1% QoQ and 26.7% YoY —-the only cost line growing faster than revenue, and the one that needs watching. Communications (32.3% of revenue, the largest vertical) grew only 1.3% YoY and fell 1.3% QoQ. Americas (48.6% of revenue) was flat at -0.1% QoQ - Q1's growth was concentrated in Europe (+8.1% QoQ, likely the large European telco deal ramp). ETR rose to 27.21% from 24.25% in Q4, driven by a ₹130 Cr deferred tax charge - the highest deferred tax provision in the data series. Two acquisitions: Avant (85% stake, ₹187.5 Cr, May 27 - provisional accounting) and Alyis from Orange Business Services (~270 employees, BRL 1.2 Mn, closed July 2 post-quarter). Satyam suspense account of ₹1,230.4 Cr remains - auditor's Emphasis of Matter continues, no new developments. Note : This is not an investment advise.

Dheeraj Kumar @DheerajK_Indian

0 Followers 3K Following

Buzz @GauravBose77

16 Followers 61 Following

Karthik @rhythmofchennai

0 Followers 102 Following

Prekshak @Prekshak23

20 Followers 1K Following

Rajesh @rkstweets

85 Followers 1K Following Avid stock market investor. Reading between the lines. Prefer value investing. Ability to hold value stocks for 5-7 years.

Jigar Shah @jigar20789

109 Followers 870 Following

Natwar Maheshwari @m_natwar

25 Followers 79 Following Enjoy Fun_tastic. Appreciate Right. Wrong is Wrong.

Vivek Shankar @viv_gb

37 Followers 684 Following

Hari Bhat @haribhat1011

348 Followers 4K Following A current affairs junkie, stock market enthusiast, ardent nationalist 🇮🇳

kamesh patel @patelkamesh

209 Followers 306 Following

ANAND PRABU J @JalkJap

0 Followers 9 Following

sarvan mugam @MugamSarva37489

29 Followers 1K Following

maani @maani54964935

113 Followers 4K Following

Momentum is my Friend @momentum_is

70 Followers 2K Following

Saurabh @sgokhales

301 Followers 4K Following

Manish Dabir @ManishDabir

67 Followers 362 Following

Rajan Trivedi @RajanTrivedi11

105 Followers 956 Following IT Professional | Investor | Learner | All tweets for education purposes

Sanjeev Gupta @sanjeevg

9 Followers 50 Following

Dhiraj Sagar (SEBI Re... @TradevisorRA

509 Followers 274 Following 📊SEBI-Registered RA (INH000015109) | Founder & CEO of Tradevisor Finnovations Pvt Ltd | Equity, Futures & Options Expert| Leading 125+ Franchises Across India.

Futures Forward @forward_futures

18 Followers 363 Following

Thezero @TheAtom0000

18 Followers 1K Following

Rhea Bhatia @_rheabhatia

502 Followers 1K Following Research Analyst, CNBC-TV18 | Defence • Agrichem • Industrials | Views personal

Balpreet Singh @balpreeetSingh

1 Followers 31 Following

Vikas Sharma @VikasSh07260842

15 Followers 424 Following

Sravana Desikan @SravanaDesikan

12 Followers 68 Following

Junaid Ali Faiyyaz @JAFaiyyaz

192 Followers 1K Following An Indian | AnIT Enthusiast | Dreamer | Husband & Father of Three Little Champs |

vsc @highgroth81

43 Followers 293 Following

vivek @vivekanandans13

28 Followers 684 Following

Deekshitha @Harishkatt25

495 Followers 235 Following Always A L'earner in Stock Market💹. Mutual fund tracker.

Neeraj Agrawal @NeerajA82753430

41 Followers 558 Following

Binham @Binhaaam

0 Followers 9 Following

Tejas shah @CaTejasshah2002

15 Followers 118 Following chartered accountant, investor, believe in generating passive income

Mukil @Mukilvenkat

1K Followers 6K Following

Vighnesh Pandit @VighneshPa60767

5 Followers 37 Following

Sunny Jariwala @SunnyJa03204025

1 Followers 120 Following

The Market Wizard @mahabul_physics

457 Followers 3K Following IIT Madras(PhD)| IITKgp(MSc)| Tweets are not buy/sell recommendations | I use this forum for my own notes|

Harnish Shukla @harnish83

7 Followers 16 Following

MOHIT SONI @mohitsonitwitt

47 Followers 770 Following Nuclear Scientist @ BARC India. l Weekend Investor. l Hear to learn and gain perspective.

Podcast Alpha @PodcastAlphaX

13K Followers 542 Following Signal. Not noise. Forensic breakdowns of the world’s most influential podcasts. Substack - https://t.co/1GNcZMJIWU DM to remove clips

The Factor Report @PeterLBrandt

1.2M Followers 2K Following Premier site for classical chart analysis of futures markets. Trader for five decades. Market Wizard. Author. Membership Factor Report https://t.co/83DcDyF2SE

Gopal Kavalireddi @gvkreddi

44K Followers 68 Following Ex-Fund Manager & Principal Officer at FYERS Asset Management | Previously with @fyers1 @SiemensGamesa, @Thermaxglobal| Views - Personal

Samir Arora @Iamsamirarora

598K Followers 41 Following

Gautam Baid @Gautam__Baid

157K Followers 374 Following PMS in India: https://t.co/VfkaWb3gub. India Fund in the US: https://t.co/hLWnq5Px9y. Book: https://t.co/BHLZ6Dju6w

Anshu Kapoor @anshukaps

852 Followers 301 Following The scale up guy: passionate about exponentially scaling up businesses that empower customers in unique ways | Technology enthusiast | Thrill seeker

Sandeep Jethwani @sandeepjethwani

9K Followers 282 Following *Wealth is built with intent.* Husband of @aswani_dipti | Co-founder @DezervHQ | Author - The Millionaire Employee | alum @iimbangalore #VJTI | 🇮🇳

Aashish P Sommaiyaa @AashishPS

55K Followers 2K Following Equity Partner & Chief Executive Officer @whiteoakcap, ex MD & CEO @motilaloswalamc & Head Retail Business @iciciprumf … under construction… always…

Raunak Onkar @oraunak

28K Followers 1K Following Kit Kat Connoisseur Research & Investment Management @PPFAS Mutual Fund. Disclaimer: All tweets are my own views and not of PPFAS. IG & Threadsapp: oraunak

NEIL PARIKH @npparikh6

38K Followers 298 Following Chairman and CEO, PPFAS Mutual Fund (Value Investing focus)

Rajeev Thakkar @RajeevThakkar

37K Followers 123 Following Life long learner (Mostly inactive account)

Vetri Subramaniam @VetriSmv

16K Followers 175 Following Tweets are not recommendations.RTs are not endorsements. Tweets are my personal opinions, not that of my employer.

Sunil Singhania @SunilBSinghania

122K Followers 443 Following Founder - Abakkus Asset Manager Pvt Ltd. Views personal, retweets not endorsements, no stock reco, might be having positions in any mentions.

Sundeep Sikka @sundeepsikka

20K Followers 461 Following Managing Director & CEO, Nippon Life India Asset Management Ltd. @NipponIndiaMF (views expressed are personal)

Kalpen Parekh @KalpenParekh

62K Followers 3K Following Heroes keep bios, not me. Views are mine. Reposts & likes are not endorsements. CEO & MD at @dspmf

Nilesh Shah @NileshShah68

602K Followers 507 Following Student of Market. believer in Mutual Fund Sahi Hai. These are my personal views. Retweet is not an endorsement of views.

Ajay Joshi Chemicals @JoshiEien

17K Followers 275 Following Official X account of AJC: Asia’s most specialised chemical sector advisory & intelligence firm Views/opinions @ CNBC, BBC, Economic Times, NDTV Profit 📍🇮🇳

Ambarish Kenghe @kenghe

2K Followers 326 Following Group CEO Angel One, ex- VP/GM Google Pay, ex-CPO Myntra, Geek (views are my own)

Niraj @cybrogsrule

95 Followers 448 Following All things @ https://t.co/u6IgQNS59a https://t.co/jpl61eeyRj

Nitin Mangal @nrmangal

19K Followers 123 Following Forensic Analysis & Corporate Governance 📊 | I find the red flags the market misses.

Tarun Dua @tarundua81

3K Followers 3K Following Chief of Entropy Reduction at E2E Networks. Building accelerated computing platform from India for the world at https://t.co/AH3v0I7BHG . Tweets Personal.

Jeremy Howard @jeremyphoward

323K Followers 7K Following 🇦🇺 Co-founder: @AnswerDotAI/@FastDotAI ; Prev: Professor@UQ; @kaggle founding president; founder @fastmail/@enlitic/… https://t.co/16UBFTX7mo

Harshjit Sethi @HarshjitSethi

9K Followers 447 Following Love what I do. Co-founder and GP at Ambition. Former early stage investor at Sequoia India/Peak XV Partners. 2x Stanford alum. Aspiring runner

Ashish Kacholia @LuckyInvest_ARK

117K Followers 2K Following Mission 500 - be part of 500 founder journeys. Not SEBI registered. Birder, Conservationist and Jungle lover - all posted pics have been clicked by me

Neil Borate @ActusDei

101K Followers 806 Following Editor-in-chief at thefynprint (Previously Personal Finance Editor, Mint)

Vishnu Kapadia @MJKinvestments

30K Followers 102 Following CIO at MJK Investments. Tweets are for educational purpose only. Find us on Instagram: https://t.co/cQFdhHNNS4

Abhishek Jain @abhishekcjain

21K Followers 492 Following Father. Husband. Views are personal. If not market then I enjoy current affairs, sports, movies, quizzes & history.

The Moat Investor @DMoatInvestor

2K Followers 122 Following Stock analysis blog. https://t.co/2rD2GjMIN3 Data driven business analysis and moat as core of investing.

Shreenidhi P @nid_rockz

201K Followers 205 Following Research Head at PINC Wealth Management CFA Level 3 candidate, MBA Finance from Great Lakes Institute of Management, Passionate about equity research

Capitalmind @capitalmind_in

49K Followers 62 Following We are a SEBI-registered PMS offering long-term wealth-building with effective investment strategies. More: https://t.co/5bJsJLyLyW Reg: https://t.co/UCIMYZB2il

Debashis Basu @Moneylifers

65K Followers 360 Following PMS:https://t.co/11W5famct6 Research:https://t.co/BMZazYkGKR https://t.co/sZ1ZtWGZKk Books:https://t.co/Mf1I9SmcLP Media: https://t.co/c0PLFUhakd

Nithin Kamath @Nithin0dha

956K Followers 187 Following Founder & CEO @Zerodha @Rainmatterin Learning at @RainmatterOrg Musings on business & life: https://t.co/gQi9cu6E5h. Views are personal, Nothing is advice.

sandip sabharwal @sandipsabharwal

128K Followers 75 Following RESEARCH ANALYST EQUITY INVESTING INH000008109 IIT Delhi & IIM Bangalore Ex Head of Equity SBI MF, CIO JM Financial Stock Market Investing

Shyam Sekhar @shyamsek

117K Followers 797 Following Making Every Investor Think Big. Taking 1 lakh investors to 1 crore. https://t.co/bdy0ybvHhZ https://t.co/1m9lpShK7K

Equity Insights Elite @EquityInsightss

62K Followers 742 Following Growth + Value Investor | SEBI Registered Research Analyst INH000021261 | Fundamental Analysis | SRCC Alum | Contact : https://t.co/6yXVi6mOff

Deepak Shenoy @deepakshenoy

289K Followers 3K Following CEO, Capitalmind Mutual Fund PMS: https://t.co/qHGwv9Fe7R Views personal, not advice Book: Money Wise https://t.co/JVSZENRUbj

ishmohit @ishmohit1

124K Followers 890 Following Keen observer of the human Behaviour| Founder at SOIC| Teacher| SEBI Registered RA |INH000012582 Courses at https://t.co/SHdiWxVVzi

kumar saurabh @suru27

110K Followers 407 Following Founder - Scientific Investing | SEBI RIA @Jaima Scientific Ventures LLP (INA000021030) | Data Science - Top 40 under 40 | Guest Faculty | Ex- EY, HP, ICRA

Intrinsic Compounding @soicfinance

281K Followers 454 Following 🏛Seeking Wisdom in the Indian Stock Markets|Disclaimer:Nothing should be considered as investment advice to buy or sell| Education|Fundamental AnalysisTrends for United States

You might like